All Stock Market Guides

Learn trading in simple and easy-to-understand chapters. Each chapter is designed to progress you toward becoming a well-informed trading enthusiast.

Articles

Technical Analysis Guide

Start your stock market journey by understanding the most foundational concept in trading – technical analysis.

Chapter 1: Introduction to Technical Analysis

If you’re here, you must have made peace with the fact that you cannot pick stocks randomly and expect to get rich one day. The stock markets don’t work that way.

You must follow a method or structure backed by reason to build wealth in the stock markets. There are many logical methods, one of the most popular ones being technical analysis.

Understanding Technical Analysis

It must be pretty clear by now that you must buy and sell the right ones at the right time to profit from stocks. But how do you know when to buy or sell a stock? And what things should you look at before choosing a stock? This is where technical analysis comes into play.

Technical analysis helps predict the directionality of financial assets such as stocks. But what is technical analysis all about? And what exactly does this mean for you as someone who wants to trade and make money through stocks?

Let us understand with a simple example.

Imagine you are a farmer. You have bought new land in another town for agricultural purposes, and you must decide which crop to plant to maximize your land’s productivity.

Option 1: Research by yourself

Imagine you try to conduct some research of your own. You might want to answer questions like:

- Based on the water conditions, which crop will suit this soil?

- What is the most appropriate crop for this climate?

- Which crop has the highest demand and will fetch a good price in the market?

After reviewing a vast checklist, you will try what seems ideal and hope for the best.

The advantage of this technique is that you will know more about the crop you are planting. However, this method will only give you an idea of what may happen, and you have to check for different crops in your limited time. Hence, there is a large uncertainty about the crop’s performance because it is based on a lot of guesswork and restricted information.

There are some advantages to this technique, too. You will have a deeper understanding of the crop you are planting. However, this method can be time-consuming, and there will be a long gestation period to determine if the chosen crop will yield the best results. The decision also risks being based on a limited set of data and personal assumptions, which may not provide the most reliable outcome.

Option 2: Learn from other who've done it

Another option to decide your crop too.

You can ask your neighbour farmers which crop they have been harvesting in the past. You will know that a particular crop has a high benefit in that area, and by following them, you can plant a crop that has worked for farmers in that area. There is a high chance that you would benefit by planting that specific crop because you’re relying on proven information from the market participants in that area.

The paramount comfort of this technique is its scalability. You need to know which crop is the best fit and has the most demand in that area. However, beware that your neighboring farmers might only sometimes be correct.

From Fields to Finance: Picking Winners

Option 1 is similar to fundamental analysis in financial markets, where you independently research the stock you buy.

Fundamental Analysis

Fundamental analysis is a way to determine a company’s actual value by examining its finances, business model, management, and the overall economy.

Option 2 is similar to technical analysis, where the idea is to select and trade stocks based on their historical data and market participants’ behavior.

Technical analysis studies market action, just like our farming analogy. You have farming tools and equipment to help you sow seeds and fertilize land. As a result, you get proper management to get the maximum yield of crops. Similarly, tools like historical price data and indicators help us estimate the market’s direction in technical analysis. Both technical and fundamental analysis solve the same problem: determining the direction in which prices will likely move. They just approach the situation differently.

Technical analysts focus on the effect, believing that the outcome is all they need to know, and do not unnecessarily consider the reasons or causes of that effect. On the other hand, fundamental analysts always seek to understand why something is happening and try to predict the factor instead of its impact.

Technical Analyst

A technical analyst studies past market data, primarily price and volume, to predict future price movements. They use charts and indicators to identify patterns and trends in the market.

Fundamental Analyst

A fundamental analyst examines a company’s financial health, such as its profits and growth, to determine whether its stock is a good investment. They study company earnings, revenue, and the overall economy to understand the stock’s value.

Like any other research technique, technical analysis has its own set of assumptions. As you trade based on technical analysis, you should know these to unleash the full potential of technical analysis.

Generally, people argue that one approach is more suitable for decoding the market. Each method has merits and demerits, and wise traders will educate themselves to look for investing and trading opportunities in the market.

Assumptions of Technical Analysis

Now that you understand the concept of technical analysis, it is crucial to know its assumptions. This approach is based on three premises:

- Markets discount everything: This assumption means that all factors—fundamental, psychological, and political—are already reflected in the market price. For example, if someone with inside information buys a lot of a company’s stock because they expect good earnings, the stock price might rise even before the announcement. This price movement hints to technical analysts that something significant will happen. Here, we are assuming that no such publicly available information is yet to be reflected in the market price.

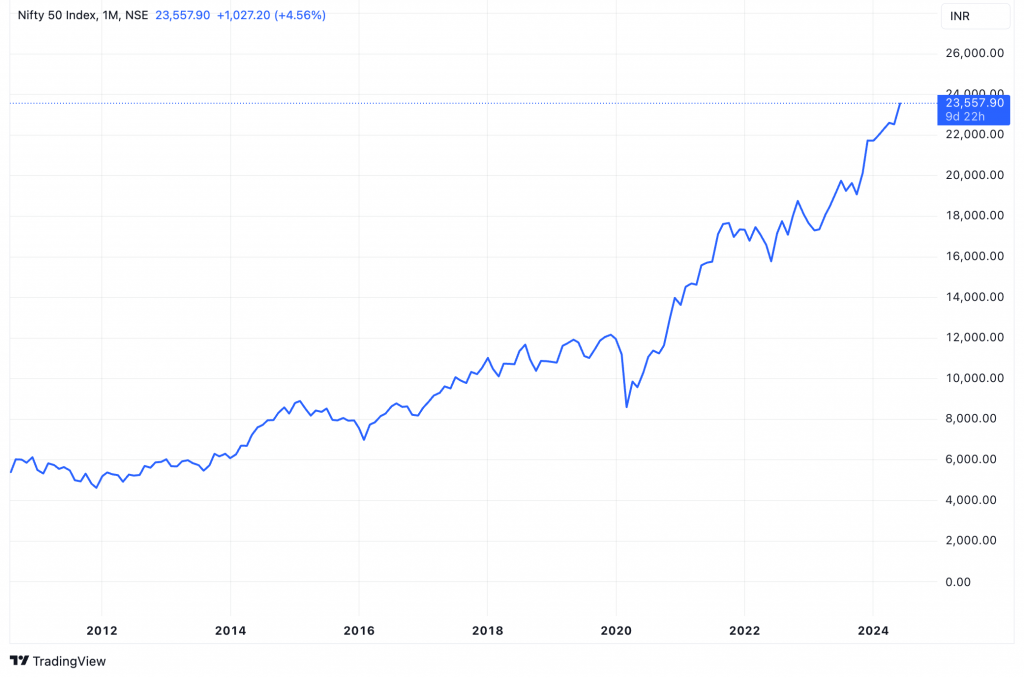

- Price moves in a trend: Market prices always follow a trend. All significant market moves are the outcome of a trend. Most techniques used in technical analysis are trend-following, meaning they intend to identify and follow existing trends. For example, the recent rise in the NIFTY 50 index is a good illustration. The index has been reaching new highs and has surged significantly this year. Once a trend is established, prices tend to move in that direction.

All Time High

An all-time high in the context of stocks is the highest price a stock has ever reached in its trading history.

Technical Analysis Fits Everywhere

One of the beauties of technical analysis is that it can be applied to any asset class with historical time series data. Time series data in technical analysis includes price information such as open price, high price, low price, close price, and volume.

Types of Prices

- Open Price: The first price at which a stock is traded when the market opens for the day.

-

High Price: The highest price at which a stock has been traded during a specific period, like a day.

-

Low Price: The lowest price at which a stock has been traded during a specific period, like a day.

-

Close Price: The last price at which a stock is traded when the market closes for the day.

-

Volume: The total number of shares of a stock that are bought and sold during a specific period, like a day.

Trading is just like learning to play guitar. Once you master the basic chords and techniques, you can play any song, regardless of the genre. Similarly, once you learn technical analysis, you can apply the concept to trade across Indian markets, such as equity, crypto, forex, and fixed income.

Fundamental Analysis vs. Technical Analysis

Technical analysis provides flexibility across asset classes, which is impossible with any other research technique. However, fundamental analysis requires studying many aspects of an asset class. And these fundamentals change with each asset class. For example, while you will have to research company financials and management commentary when analyzing companies, you will have to check factors such as rainfall, harvest, demand, supply, inventory, etc., while studying commodities. On the other hand, technical analysis will remain the same. It is independent of the asset you are studying. We can apply the same technical indicator to various asset classes because it’s primarily about historical data.

Annual Report

An annual report is a detailed document that a company publishes yearly to show its financial performance and activities. It includes information about how much money the company made and spent, what it owns and owes, and its plans for the future. It helps investors understand the company’s performance, history, and future plans.

Can Technical Analysis be Used Across Time Frames?

Another strength of technical analysis is its ability to handle different time frames. The same principles apply when trading minute-by-minute changes for intraday or focusing on longer-term trends. Some believe this technique is only valid for short-term analysis, but that’s not true. It can also be very effective for long-term forecasting. Using weekly and monthly charts that span several years, you can successfully apply technical analysis for long-term predictions, just as you do for short-term trades.

Intraday

Intraday means within the same trading day, i.e., buying and selling a stock between market opening and closing.

When to Use Technical Analysis and When Not TO

Market players often see technical analysis as an easy way to earn money in the stock market because it involves identifying patterns and making trading opportunities for them. However, one must try to learn the technique to reach that stage.

Before diving deeper into this technical analysis guide, it’s essential to understand when and when not to use technical analysis.

When to use technical analysis

- Short-term trading: Technical analysis is ideal for intraday or swing trading because it mainly helps capture quick gains based on short to medium-term trends.

- Identifying entry and exit points: Technical analysis reads price and volume to determine the directionality. It helps traders decide when to enter and exit trades by identifying patterns and signals that indicate potential price changes.

- Volatile and liquid markets: Technical analysis helps traders get more accurate signals in volatile markets where fundamental analysis might be less meaningful to deploy. For instance, forex markets have very high liquidity and volatility, and there is historical proof that technical analysis generates decent returns there.

Volatile

A market or stock is considered volatile when its prices change quickly and unpredictably, often with large swings up or down.

Liquid Markets

A liquid market is one where assets can be quickly bought or sold without causing a significant change in their price, typically because there are many buyers and sellers.

When to not use technical analysis

Just like you learned when to use technical analysis, you should also know when not to…

- Not Suitable for Long-Term: Fundamental analysis is more suitable for long-term investments because, over long periods, factors like a company’s fundamentals, industry trends, and overall economic conditions have a more significant impact than price trends. These long-term trends are guided by underlying factors, which fundamental analysis aims to determine. Let’s understand this with TCS, short for Tata Consultancy Services, an IT company whose stock trades on Indian exchanges.

Technical analysis doesn’t always work…

Take Tata Consultancy Services (TCS), a leading IT company in India. You’d choose to invest in TCS for its long-term growth, strong earnings, and solid business model. However, in the short term, regulatory concerns might arise. Technical analysis might signal a short-term decline, helping you avoid buying TCS at a lower value and suffering a loss. So, from a long-term perspective, fundamentals typically play a vital role in the price of assets.

2. Unpredictable Events: Technical analysis offers little help in predicting and capturing profits from significant news events, such as election results, geopolitical issues, or economic events, like changes in GDP and interest rates, because market sentiment shifts suddenly. Thus, technical analysis of stocks is of little use in these situations.

3. Illiquid Markets: Technical analysis often fails in low-liquid assets because low trading activity makes assets easy to manipulate, rendering the logic of technical analysis meaningless. Here, general patterns or indicators of technical analysis don’t work.

In the next chapter, we’ll explore how stock prices fluctuate and learn how to read and interpret them for effective trading.

Summary

1. Technical analysis helps determine the future direction of financial assets using historical data, such as price and volume.

2. This method can be applied to various assets as long as historical data is available, making it adaptable to different time frames.

3. Technical analysis is based on a few core assumptions:

- Markets discount everything: All factors are reflected in the market price.

- Price moves in trends: Significant market moves follow established trends.

- History tends to repeat itself: Price trends repeat due to consistent human psychology.

4. In liquid markets, technical analysis identifies short-term trading opportunities but is less suitable for predicting uncertain events and determining asset values in the long term.

Chapter 2: Types of Stock Price Charts

As we learned, technical analysis is like predicting the future by looking at the past. It assumes that prices follow trends, history repeats itself, and the market tells all. In this chapter, we’ll explore the exciting world of different types of stock price charts, such as line charts, bar charts, and candlestick charts. We’ll also understand the different types of prices: open (O), high (H), low (L), and close (C).

You may wonder why we need charts in the first place. Charts help us clearly see price movements over time, making it easier to spot trends, patterns, and trading opportunities. Since technical analysis requires four data points to be displayed simultaneously for a complete view of price movements, charts also provide a clear picture of the market’s behavior, helping traders make informed decisions.

This chapter will focus on the different types of charts, especially Japanese candlestick patterns, which are one of the most loved chart types. But before that, we’ll look at the pros and cons of other charts to understand why candlesticks are so popular.

Trade Summary

Before we discuss the formation of different types of charts, let’s consider the different types of prices a stock trades at during a regular market day.

The Indian stock market is open from 9:15 AM to 3:30 PM. During these market hours, numerous trades occur throughout the day. Tracking all of these price movements is impossible for a trader. One needs a summary of the trading action that points to the important stuff, not the details on every price point.

Let’s understand what the open, high, low, and close prices are using a real-life example of Reliance Industries’ stock price:

- Open Price: The price at which Reliance Industries’ stock trades first when the market opens at 9:15 AM. For example, on June 7th 2024, the opening price was ₹2,857.

- High Price: The highest price at which Reliance Industries’ stock is traded during the day, between 9:15 AM and 3:30 PM. On June 7th 2024, the high price was ₹2,944.

- Low Price: The lowest price at which Reliance Industries’ stock is traded during the day, between 9:15 AM and 3:30 PM. On June 10th 2024, the low price was ₹2,853.

- Close Price: The price at which Reliance Industries’ stock is traded when the market closes at 3:30 PM. On June 10th 2024, the closing price was ₹2,940.

The trading session is considered ‘positive’ if the closing price is higher than the opening price, like in this case (₹2,940 close vs. ₹2,857 open). It is considered ‘negative’ if the closing price is lower than the opening price.

We use these prices to plot charts, which help us analyze future price movements. But let’s first understand why are charts so useful in the first place.

Why Traders Love Charts?

The chart is a price sequence plotted over a specific time frame, typically with a price scale on the y-axis and a time scale on the x-axis. Charts mainly help see past price movements, which in turn help us predict future price movements. Technical analysts use charts to analyze various securities and forecast future price movements. Charts also help fundamental analysts because they show how a company’s stock price reacts to its financial health.

Security

In finance, security is a claim that you can buy, sell, or trade, like a stock or bond. Stocks represent owning a part of a company, while a bond is a certificate of lending to the company with a promise of repayment with interest. Securities represent financial interest and let you earn from either ownership or lending.

Let’s explore the different types of charts and learn how they can be used.

Line Chart

The most basic chart type is a line chart because it uses only the closing price of the stock price or index over a defined period to form the chart. On the chart, a dot is plotted on a specified period, that is, the closing price, and then these dots are connected, forming a line that is plotted across a specific period of time.

The advantage of a line chart is that it is simple and easy to understand, and a trader can identify general security trends over long periods of time like weeks, months, or years. The disadvantage is that they do not provide additional details besides closing prices, ignoring the open, high, and low prices. Though closing prices are useful,traders prefer seeing more information, taking us to the next type of chart.

Bar Chart

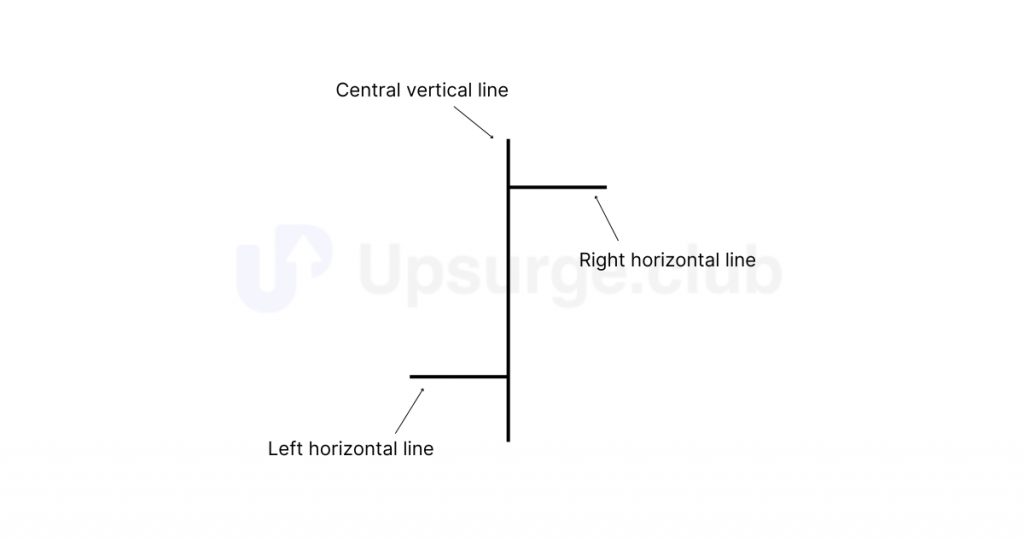

A bar chart is more flexible than a line chart because it considers all price types: open, high, low, and close. A bar chart looks like this and has three components:

Here is a table summarizing what the different lines mean in a bar chart:

| Line | Meaning |

|---|---|

|

Central vertical line

|

The price range of the security during a specific period. The top of this line is the high price, and the bottom is the low price.

|

|

The left horizontal line |

Shows the price at which the security started trading in that period, i.e., opening price. |

|

The right horizontal line |

Shows the price at which the security traded at the end of that period, i.e., closing price. |

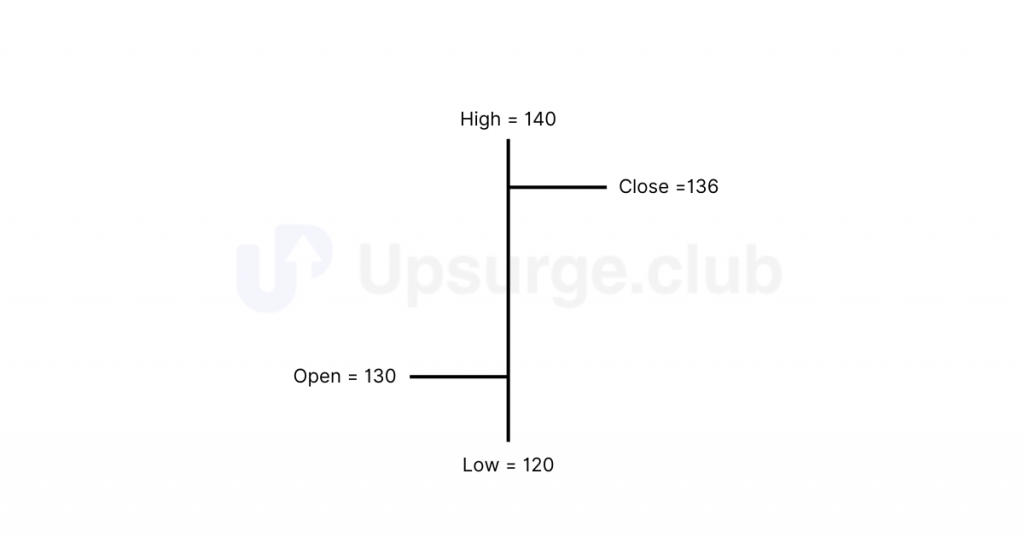

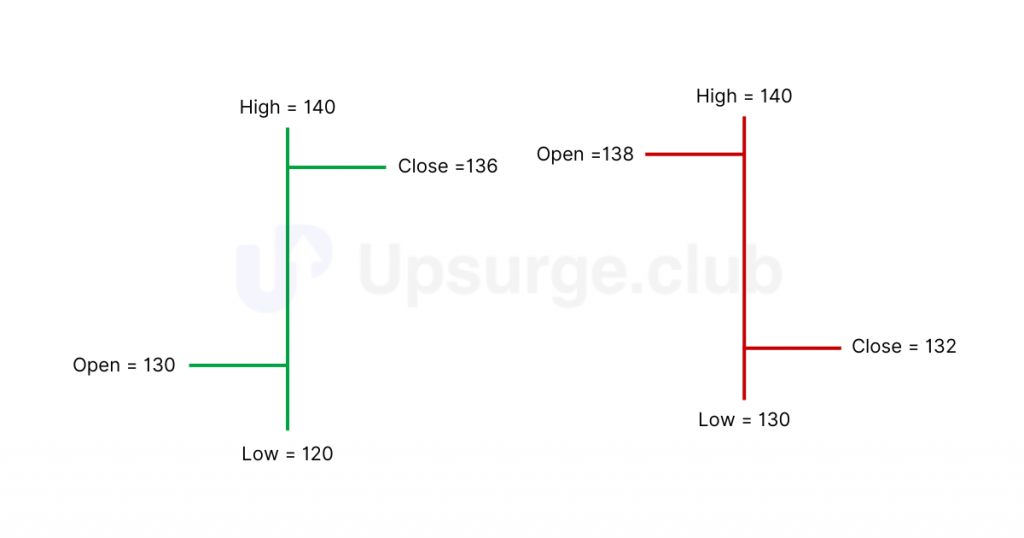

Let’s understand with an example. Assume OHLC (open, high, low, close) price data for a stock as follows:

Open – 130

High – 140

Low – 120

Close – 136

For the above data, the bar chart would look like this:

Here, you can see that we can plot all price types over a specific period in a single bar. Hence, if we create one bar for one day, we will have five vertical bars to view a five-day chart. Here is how a bar chart looks:

If the left horizontal line, which represents the opening price, is lower than the right horizontal line, i.e., the closing price, then it is a positive day for the markets, called a bullish day. A bullish day is typically represented by a green or blue bar.

If the left horizontal line, which represents the opening price, is higher than the right horizontal line, i.e., the closing price, then it is a negative day for the markets, called a bearish day. A bullish day is typically represented by a red or black bar.

Here is a snapshot of both types of bars:

The bar chart displays all four data points, but its disadvantage is that it lacks visual appeal. It is difficult and tedious to spot potential patterns when looking at a bar chart, especially the opening and closing prices. Analyzing bar charts in multiple time frames becomes more challenging.

Some traders prefer bar charts, so they are worth mentioning. However, most traders prefer Japanese candlesticks, the default option for most charting tools.

So, let’s dive deeper into them.

Lighting Up Your Trading Game with Candlesticks

In the 18th century, Homma discovered that by observing rice’s opening, closing, high, and low prices, he could identify patterns that predicted future price movements. This method allowed him to gain insights into market psychology and price action.

Although candlesticks have been used in Japan for centuries, western traders were unaware of them until the 1980s when Steve Nison introduced them in his book, “Japanese Candlestick Charting Techniques.” Following the book, many candlestick patterns retain their original Japanese names, adding an oriental touch to technical analysis.

Understanding a Candlestick

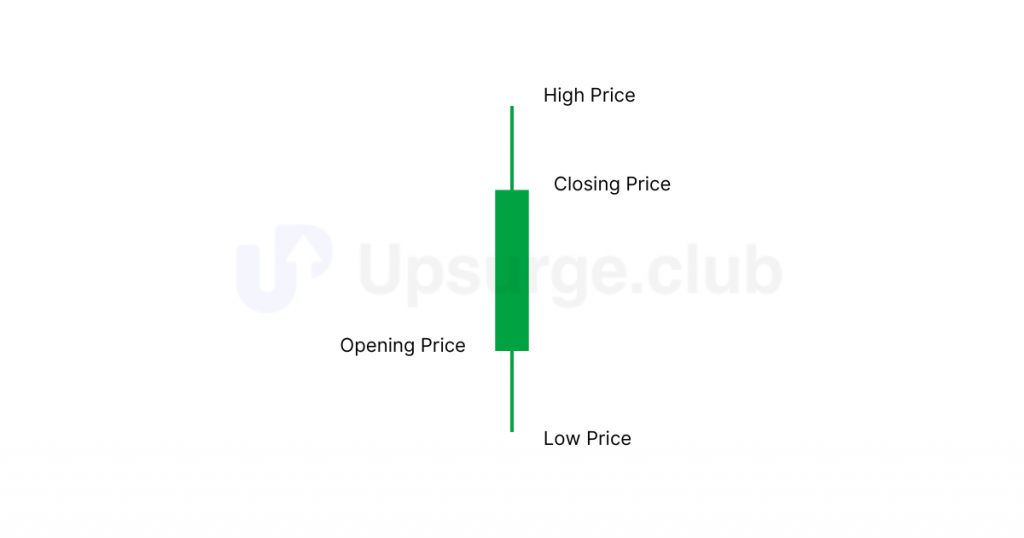

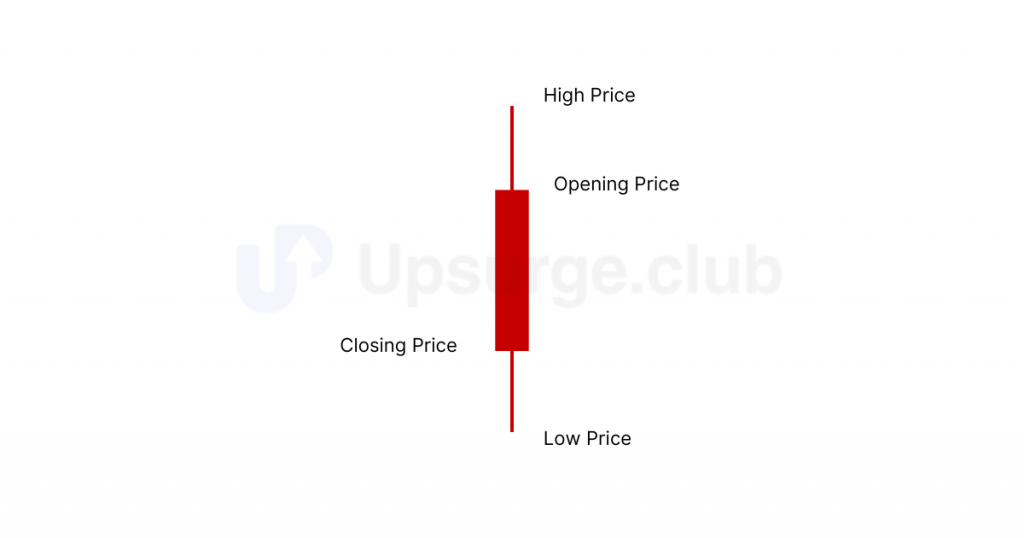

You have seen the bar chart, which shows opening and closing prices by a tick on the left and right of the bar, respectively. However, in a candlestick chart, the opening and closing prices are displayed by a rectangular body, and the high and low prices are displayed using wicks.

The candlestick, like a bar chart, is made of 3 components. Let’s look at how a bullish candlestick looks:

- The central body – The thicker, rectangular body connects the opening and closing price.

- Upper shadow – Connects the high price to the opening or closing price, whichever is greater.

- Lower Shadow – Connects the low price to the opening or closing price, whichever is lesser.

Here’s how a bullish candlestick looks:

Conversely, here’s how a bearish candlestick looks:

The candlestick chart takes shape by plotting them in a time series: green candles indicate bullishness, and red candles indicate bearishness.

In summary, candlesticks are easier to interpret than bar charts. They help you visualize the relationship between the opening and closing prices and the high and the low prices more clearly than any other chart type.

Interpreting Candlesticks

Candlesticks are super important because they help us predict market trends. They can show if prices will form trends that go up (bullish), down (bearish), or stay the same (sideways). Let’s check out each one!

- Bullish Trends (Uptrends): An uptrend is when prices rise. A bullish trend can be spotted when several candlesticks form consecutively higher, often with most candlesticks being green.

- Bearish Trends (Downtrends): A downtrend is when prices decline. A bearish trend can be spotted when you visit several candlesticks being formed consecutively lower, often with most candlesticks being red.

- Sideways Trends (Consolidation): A sideways trend is when prices remain within a small range over time in a narrow range, indicating little to no movement. This happens when multiple candles on a chart form at about the same level, neither going up nor down.

Now that you have understood candlesticks and their versatility, let’s examine other types of non-candlestick charts as well.

Some Other Useful Chart Types

While Japanese candlestick charts are widely used for their versatility, other charts like point and figure, Renko, and Heikin-Ashi charts are also crucial for analyzing trends. These charts offer unique perspectives that can enhance a trader’s understanding of market movements, helping to create a more comprehensive view of price action and trends.

Let’s learn a little about each one of them.

Point and figure charts focus solely on price movements, using Xs and Os to indicate rising and falling prices while ignoring time. This method filters out minor price fluctuations, making identifying major trends easier. However, the downside is that these charts can miss detailed price action since they do not consider the time factor.

As you have seen, you can use different charting types to your advantage, depending on your objective. However, Japanese candlesticks are widely used because of their versatility and simplicity. Here’s a table summarizing the pros and cons of each chart type:

| Chart Type | Pros | Cons |

|---|---|---|

|

Bar Chart |

Shows all price types (open, high, low, close), good for detailed analysis

|

Not very visually appealing, hard to spot patterns quickly |

|

Candlestick |

Easy to read and understand, shows market sentiment with color |

Can look cluttered, might give insufficient context

|

|

Point and Figure |

Filters out small price changes, highlights big trends

|

Ignores time, can miss detailed price movements

|

|

Renko |

Simplifies trends, reduces market noise |

Updates slowly, can miss short-term price changes

|

|

Heikin-Ashi |

Makes trends clearer, reduces small price fluctuations

|

Lags behind real-time changes, can hide immediate price signals

|

The leading reason traders prefer candlestick charts is that they are easily read and visually apparent. It shows crucial information in a simple format, making it easy to spot trends and patterns. Candlesticks reflect market sentiment with color, helping traders understand the market’s mood. Their versatility allows other tools to be used on top of them for a more comprehensive view and valuable analysis.

Trading Time Frames: Your Secret Weapon

When studying how stock prices move, a time frame is the duration of the candlestick you choose to examine. A candlestick can represent the trading activity of a day, week, month, year, or even minute. Choosing the right time frame is crucial in your trading game because it helps you understand different market trends.

The most common time frames used by technical analysts are:

- Monthly candlesticks

- Weekly candlesticks

- Daily or end-of-day candlesticks

- Intraday candlesticks like 30 minutes, 15 minutes, and 5 minutes

Look at the stock price of HDFC Bank and see how its chart differs in different time frames.

The monthly chart (2007-2024) shows HDFC Bank’s long-term trends over 17 years, as you see the four different time frames. The weekly chart (May 2020-June 2024) captures medium-term trends over four years. The number of candles increases when the time frame reduces.

Now, let’s uncover which time frame is suitable for you.

How to Pick Your Ideal Time Frame for Trading

Choose a time frame that fits your investment goals, market volatility, personal schedule, and trading time availability.

An individual must align the time frame with their trading style and goals. Intraday charts suit short-term traders aiming for quick gains, while long-term investors seeking sustained growth often rely on monthly or weekly charts.

Market volatility also plays a role. For instance, shorter time frames capture rapid price changes in high-volatility markets, while more extended time frames are better for stable markets. One should also consider the time they can give for trading because shorter time frames require more frequent monitoring, which may not be feasible for those with limited availability.

So, choose a trading time frame that matches your goals, market volatility, and availability. Here’s a table summarizing various time frames and when they should be used

| Time Frame | Useful When | Suitable For |

|---|---|---|

|

Monthly

|

Identifying long-term trends and major

market cycles |

Long-term investors |

|

Weekly |

Spotting medium to long-term trends |

Swing traders |

|

Daily |

Analyzing price movements over a period of a few days/weeks |

Swing traders and long-term investors |

|

Intraday |

Detailed views of price movements within a single trading day need to be seen |

Intraday traders |

Swing trader

Swing traders buy and sell stocks to profit from short-term price changes, usually holding them for a few days or weeks. We’ll learn more about swing trading in further chapters.

Traders also combine other time-frames to get a comprehensive of the market. Let’s look at that.

Blending Time Frames for Trading Success

You do not necessarily have to stick to one time frame. You can look at different time frames for trade objectives or even at multiple time frames to get a wider perspective of a stock price’s movement.

To identify the overall trend, you can look at longer time frames, such as daily or weekly. Then, you can switch to shorter time frames, such as hourly or 15-minute charts, to identify entry and exit points in the market. Generally, this method is helpful to avoid false signals and confirm trends. Here’s how it can work.

Let’s get an idea of how this works.

A trader notices HDFC Bank’s stock rising on the daily chart, moving from ₹1,400 to ₹1,450 over the past week. This shows a strong upward trend. The trader switches to a 15-minute chart to find a good buying point.

The 15-minute chart shows that HDFC Bank opened at ₹1,455 but then dipped to ₹1,450. This dip can be seen as the stock price briefly returning to its average level before continuing to rise, a concept known as mean reversion.

Seeing this brief dip within the overall uptrend, the trader buys shares at ₹1,450. They increase their chances of success by aligning their short-term trade with the long-term trend and considering the mean reversion.

Using multiple timeframes and the idea of mean reversion, the trader makes a well-rounded decision, reducing the risk of false signals and improving the likelihood of a successful trade.

Summary

- The different types of prices in a defined period – Open, High, Low, Close

- Open Price: The first price at which a stock is traded when the market opens for the day.

- High Price: The highest price at which a stock is traded during a specific period, like a day.

- Low Price: The lowest price at which a stock is traded during a particular period, like a day.

- Close Price: The final price at which a stock is traded, serving as a reference point for the next day.

- Different chart types used in technical analysis include:

- Line Charts: Simple and easy to understand, using only closing prices.

- Bar Charts: Show all price types (open, high, low, close) without visual appeal.

- Candlestick Charts: Preferred by traders for their visual clarity and ability to show market sentiment.

- Japanese candlestick charts are highly favored for their versatility, ease of interpretation, and ability to highlight trends and market sentiment effectively.

- Other Chart Types and Their Characteristics:

- Point and Figure Charts: Focus on price movements and ignore time, making them suitable for spotting major trends but lacking detailed price action.

- Renko Charts: Renko charts use bricks to simplify trends. They effectively highlight trends but can be slow to update as they only form a new brick when the price moves by a specific amount.

- Heikin-Ashi Charts: Heikin-Ashi charts smooth out price data, making trends more apparent. The average price data reduces market noise, but this smoothing causes a lag in real-time changes.

- Select a timeframe that aligns with your investment goals, matches the market’s volatility, and fits into your personal schedule for effective trading.

- Combining longer timeframes (daily or weekly) with shorter ones (hourly or 15-minute) helps identify overall trends and find precise entry/exit points, reducing the risk of false signals.

Chapter 3: Single Candlestick Patterns - Part 1

We have learned that candlestick charts are a better way to interpret market movements than any other chart type. So, in this chapter, we will discuss the most prominent single candlestick patterns that can help us understand these movements better to take a trade.

As the name suggests, single candlestick patterns are formed by just one candle. The trading signal is generated based on a single-period trading action. Trades based on single candlestick patterns can be highly profitable, provided the patterns are identified, rules are followed, and the trade is correctly executed.

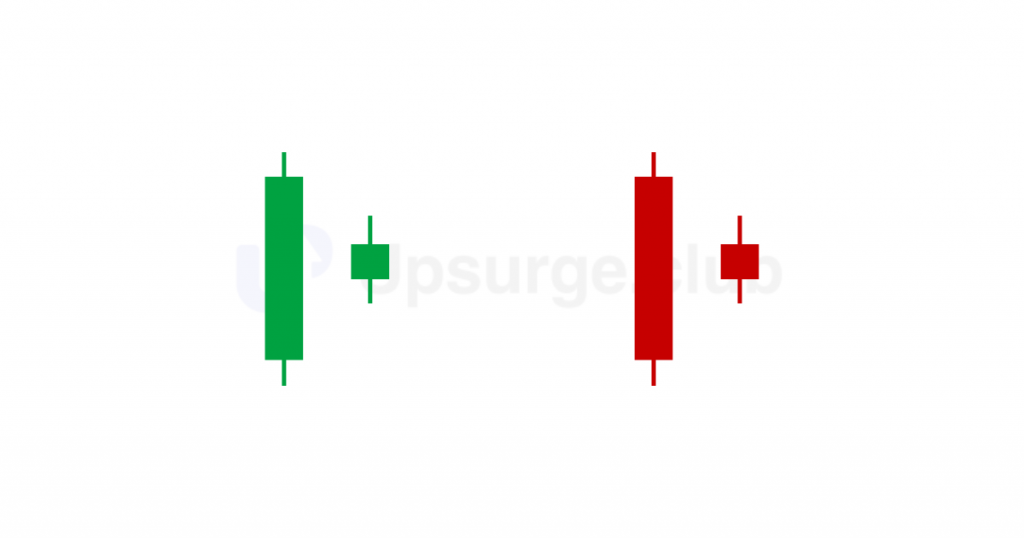

Another crucial factor to consider while trading based on candlestick patterns is the length of the candle. One candlestick shows the day's trading activity. Generally speaking, the longer the body, the more intense the buying or selling pressure. Conversely, short candlesticks indicate little price movement and represent consolidation. Here is an image depicting candles with long and short bodies, respectively:

Candlestick Trading Rules

Before we delve into single candlestick patterns, we must remember a few rules that must be followed.

Buy strength, sell weakness

The universal stock market rule says, “Buy low, sell high”. A bullish (green) candle represents a price strength, and a bearish (red) candle represents weakness. Hence, we must ensure it is a green day when we are buying, and whenever we are selling, ensure it’s a red candle day.

Be flexible with patterns

While the textbook definition of a pattern could state specific criteria, minor changes due to market conditions could occur. So we have to be flexible. However, one must be flexible within limits, so quantifying the flexibility is always required.

From now on, we will discuss the different single candlestick patterns. Let’s start with a simple but powerful pattern: the Marubozu.

Marubozu

How does a bullish marubozu form?

A bullish marubozu is a candle whose:

- The closing price is greater than its opening price

- The opening price is equal to the low price, and

- The closing price is equal to the high price.

Whenever a candlestick with the above characteristics occurs, a bullish marubozu is said to be formed. Irrespective of prior trends, a bullish marubozu indicates strong bullishness in the market. It may look like this:

A bullish marubozu signifies enormous buying pressure in the market. Considering a daily chart, market participants are willing to buy from the start of the day until the market closes for trading. This shows buyers have gained control of the market, and the overall market sentiment is bullish.

How to trade a bullish marubozu?

As traders, we should seek buying opportunities since the market outlook has turned bullish with the appearance of the marubozu candlestick. This bullish sentiment is anticipated to persist for the subsequent few trading sessions.

Ideally, a trade can be entered on the same day the marubozu is formed, just before the market closes at 3:20 PM. Still, the bullish marubozu must be validated by checking that the candle’s high equals the stock’s current market price (CMP). If these conditions are met, we will confirm that a bullish marubozu is formed, and we can go long on the stock.

Long

Going “long” on an asset means buying and holding it because you expect its price to increase. This involves purchasing stocks, bonds, or other securities to sell them later at a higher price for a profit. It reflects a positive outlook on the asset’s future performance.

- Entry point: Enter the trade at or just below the close of the bullish marubozu candle.

- Confirmation: An uptrend is confirmed if the next candle is bullish and breaks the high of the marubozu. If you prefer a more risk-averse approach, you can also enter here.

- Stop loss: A stop loss can be placed below the low of the bullish marubozu candle to limit potential losses.

Let’s understand with an example trade in Infosys.

Here, first, we will validate the physical characteristics of a candle as highlighted in the image.

Open = 1414

High = 1427

Low = 1413

Close = 1426

As we know, a bullish marubozu’s opening price should equal its low price, and a high price should equal its closing price. Although the opening price does not match its low price, there is hardly any difference between them. Remember that there can be minor variations in candlestick patterns, and we must be flexible as long as the logic of the concept holds.

Based on our method, the trade setup for the above Infosys stock would be as follows:

Entry price = Between 1427 and 1430

Stop Loss = 1413

But if we want to confirm the formation of a bullish marubozu or have a risk-averse approach, we must wait until the next day. The downside is that buying the next day results in a much higher purchase price and a deeper stop loss.

In our example, buying Infosys on the same or the next day would have been profitable.

Here is another example of a bullish marubozu pattern and a resulting uptrend:

The above example of HDFC Bank shows that it would have been profitable here if we had bought this stock on the same day or the next day. However, there will be some cases where marubozu candlesticks fail, like the one below:

After a bullish marubozu formed on Reliance’s stock, a downtrend resulted. Hence, remember that not every marubozu is foolproof, and having a stop loss can help you deal with such situations.

Now, let’s move on to the bearish marubozu.

Bearish Marubozu

How does a bearish marubozu form?

As a bullish marubozu indicates a strong sentiment of bullishness, the bearish marubozu reflects bearish sentiment in the market, and it is formed when a candle’s

- The closing price is less than its opening price

- The opening price is equal to its high price

- The closing price is equal to its low price

This candlestick indicates selling is done for each price point throughout the day. It does not matter what the prior trend has been; the action on the marubozu day suggests that the sentiment has changed, and the stock is now bearish.

In the above chart of Asian Paints, a bearish marubozu pattern is formed after a significant drop in the stock. If we look at the OHLC data,

Open = 3563

High = 3563

Low = 3378

Close = 3378

As mentioned before, a slight variation in OHLC is acceptable up to a specific limit.

Typically, for a marubozu candle, the open and high (for bearish marubozu) or open and low (for bullish marubozu) can have a slight difference, generally not more than 1% of the stock's price. We use this 1% limit because it ensures the candle still clearly indicates strong selling (or buying) pressure without significant price fluctuations, which might otherwise weaken the reliability of the marubozu pattern.

For example, if the stock price is 3563, a 1% variation would be about 36 points. So, if the high were slightly higher at 3599, it would still be considered a valid marubozu pattern. This 1% limit maintains the integrity of the marubozu pattern by ensuring it accurately reflects market sentiment.

How to trade a bearish marubozu?

A trader should look out for shorting opportunities in the market because sudden changes in sentiment will be carried forward over the subsequent few trading sessions.

- Entry Point: Enter the trade at the close of the bearish Marubozu candle or the opening of the next candle.

- Confirmation: Confirm the downtrend by checking if the next candle breaks the marubozu low. If you prefer a more risk-averse approach, you can also enter here.

- Setting Stop Loss: Place the stop loss at the high of the Marubozu candle to limit potential losses if the trade goes against you.

Let’s look at an example in HDFC Bank’s stock:

When the Pattern Falls Short

Earlier in this chapter, we discussed why a candle’s length is essential. We should avoid trading when the candles are small because they show low trading activity. Small candles make it hard to predict market movement because they indicate that prices are the same, making it unclear how the market is going. With fewer people trading, price signals are less reliable, increasing overall volatility.

Here is an example from the Tata Motors Ltd. chart:

For this reason, one should avoid trading in too short candles.

Let’s move on to the second candlestick pattern – the Doji.

Doji

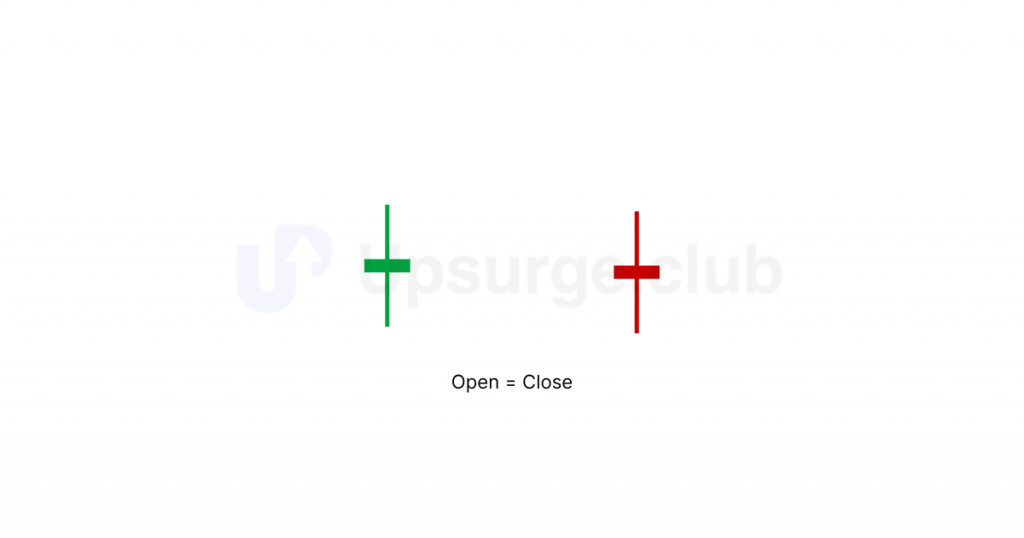

How does a doji form?

A Doji is formed when

- The opening price of a candle is equal to the closing price.

The upper and lower wicks can be of any length, resulting in the cross, inverted cross, or plus sign. It is a vital candlestick pattern that tells us about market sentiment. The word “doji” refers to both the singular and plural forms.

Though bullish and bearish dojis signify roughly the same sentiment, here’s a pictorial representation of the candlestick:

A doji conveys a sense of indecision or tug-of-war between buyers and sellers. Prices move above and below the opening level during the session but close at or near the opening level. The result is a standoff. Neither bulls nor bears could gain control, and a turning point could develop.

A doji can signal different things based on its place in the trend, making it a vital pattern to watch. Let’s discuss each one.

Doji in an uptrend

The relevance of doji depends upon the preceding trend or preceding candlesticks. The formation of doji after an uptrend or a long green candlestick shows that buying pressure is weakening. After a downtrend or a prolonged red candlestick, a doji signifies that selling pressure is easing.

Dojis indicate that supply and demand are balancing, and a trend change may be near. Dojis alone don’t confirm a reversal; further proof is needed.

Let’s look at the daily chart of the Infosys Ltd. chart.

Here, the doji appears after a healthy uptrend, after which the stock reverses its direction and corrects.

Doji in a downtrend

After a decline or long red candlestick, a doji shows that selling pressure might be easing, and the downtrend could end. Though the bears are losing control, more strength is needed to confirm a reversal.

The chart shows an initial downtrend, indicating a period of selling pressure for HDFC Bank. Following this, several doji candlesticks suggest indecisiveness in the market, as buyers and sellers have a definitive upper hand. After this period of indecision, the buyers are marking a significant upward movement.

So, the next time you see a doji individually or in a cluster, remember that the market is indecisive. The market could swing either way, and you need to build a stance that adapts to the expected movement.

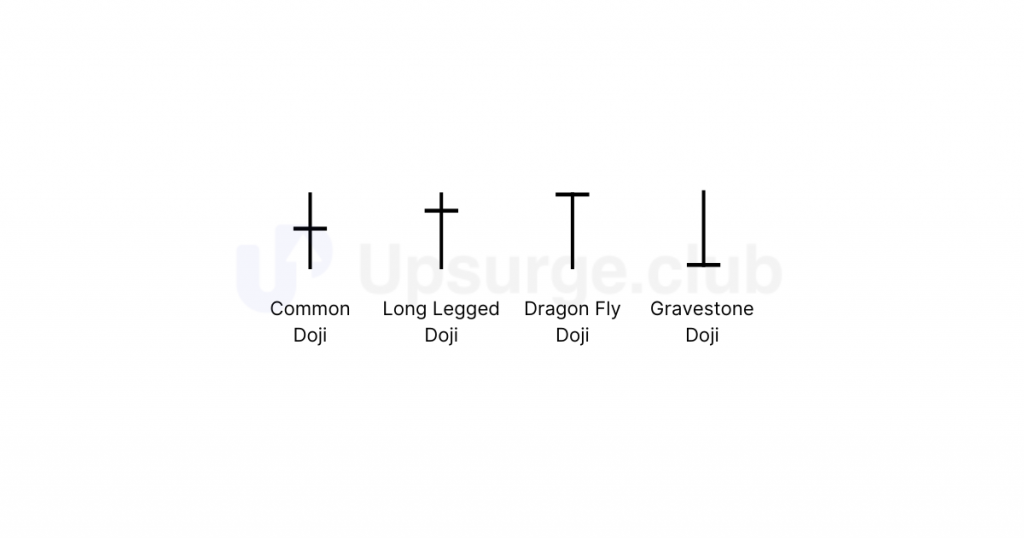

Other types of doji candles also exist, depending on their shape and size. Let’s decode each one.

- Long-Legged Doji: These candles have long upper and lower shadows almost equal in length. These reflect a significant amount of indecision in the market. Long-legged doji indicate that prices traded well above and below the session’s opening level but closed virtually even with the open. After much noise and commotion, the outcome was almost the same as the beginning of that day.

- Dragonfly Doji: A Dragonfly Doji forms when the open, high, and close prices are the same, creating a long lower shadow. The candlestick resembles a “T” because there is no upper shadow. This pattern indicates that sellers controlled the session, pushing prices down, but by the end, buyers returned and brought prices back up to the opening level. A Dragonfly Doji suggests a potential reversal or shift in market sentiment.

- Dragonfly Doji in a Downtrend: In a falling market or near a low point, this pattern can suggest a possible turnaround to higher prices.

- Dragonfly Doji in an Uptrend: In a rising market, a Dragonfly Doji means buyers tried to push prices up, but sellers were still strong. After a good rally, this pattern suggests a price drop. We need more proof to confirm this change.

3. Gravestone Doji: This candle’s structure is inverted to dragonfly doji, resulting in an upside-down “T” due to the lack of a lower shadow. It is formed when the open, low, and close are equal. The psychology behind this candle is that sellers had resurfaced by the end of the day and pushed prices back to the opening level and the session low.

- Gravestone Doji in a Downtrend: After a long downtrend, a long black candlestick, or near a low point, the focus shifts to the buying pressure, suggesting a potential bullish reversal.

- Gravestone Doji in an Uptrend: Gravestone Doji shows a failed rally despite some buying pressure in a rising market. Near a high point, this pattern suggests a potential bearish reversal.

Here’s an image representing all types of Doji

In the next chapter, we will study the hammer candlestick pattern and its different variations. We will also understand how to set targets while trading with single candlestick patterns.

Summary

1. A single candle represents day trading activity. The length of the candle is very crucial. Longer bodies indicate stronger buying or selling pressure, while shorter ones indicate consolidation.

2. A marubozu candlestick does not have an upper or lower wick, which indicates strong momentum on either side.

- Bullish marubozu candle’s open = low, close = high, shows bullishness

- Bearish marubozu candle’s high=open, low=close,showing bearishness

3. A doji candlestick represents indecisiveness in the market. One should also consider the preceding candle to anticipate future market sentiment.

Chapter 4: Single Candlestick Patterns - Part 2

This chapter will focus on the four candlestick patterns: hammer, inverted hammer, hanging man, and shooting star.

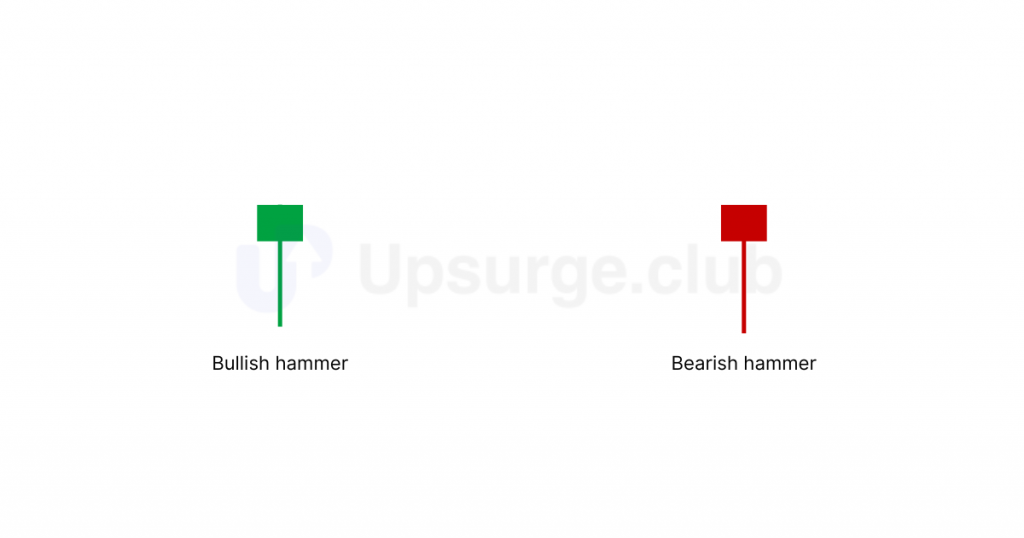

Hammer

How does a hammer form?

A hammer is a significant candlestick pattern that is formed after a downtrend. It is formed when

- The closing price is near the high,

- The opening price is near the high, and

- There is enough gap between the closing price (in case of bearish) or opening price (in case of bullish) and the candle’s low.

The longer, the lower the shadow, the more bullish the pattern. Here is how a hammer may look, whether bullish or bearish.

A hammer candlestick pattern forms when sellers push the price down, but buyers step in and drive it back up, showing strong buying interest and a potential reversal. The color of a hammer doesn’t matter much because its shape indicates a possible reversal. The key is the shadow-to-body ratio. The natural body of a hammer candlestick should be small compared to its long lower shadow, which should ideally be at least twice the length of the natural body.

Let’s understand the above chart. Tata Motors faced a significant decline with sellers in control. Each day, the stock opens and closes lower than the previous day’s close, making a new low. When the hammer candlestick is formed, some buyers step in and start buying the stock, pushing it to near the day’s high.

The hammer’s occurrence shows that buyers are trying to stop the stock from falling further and becoming somewhat successful. This has resulted in a bullish market sentiment, making it an excellent time to look for buying opportunities.

How to trade a hammer?

The trade setup for the hammer candle is that we should go long if it occurs after a downtrend, entering at the closing price of the hammer and keeping the stop loss as low as the hammer.

- Entry: Enter a long position at the opening of the candle that forms after the hammer.

- Confirmation: A hammer is more reliable in a downtrend if the next candlestick shows a higher close, indicating a potential bullish reversal.

- Stop Loss: Place a stop loss below the low of the Hammer candle to limit potential losses if the trade goes against you.

For instance in the chart of Tata Motors Ltd. below, the buying price is the closing of stock, at 391, and the stop loss is placed at 376. As the above candle has a slight upper wick, we can consider it as a hammer according to the second candlestick rule (be flexible). In the below trade, we would have been profitable.

Hanging Man

How does a hanging man form?

A hanging man is nothing but a hammer pattern appearing an uptrend. It is formed when

- The opening price is almost similar to the higher price,

- The closing price is nearly identical to the higher price,

- There is enough gap between the closing price (in case of bearish) or opening price (in case of bullish) and the candle’s low.

A hanging man signals a market high. The market is in an uptrend, signaling a bullish trend. The bears entered after the hanging man’s formation, depicted by a longer lower shadow. The entry of bears signifies that they are trying to break the stronghold of bulls. Forming after an uptrend, this candlestick pattern signals selling pressure.

A hanging man helps traders to set up directional trades. The color of the candlestick does not matter much, but the crucial thing we must consider is a shadow-to-accurate body ratio, where the length of the shadow should be at least double the size of the body.

Let’s look at the example of the hanging man below:

In the above chart of Asian Paints Ltd., a significant downfall can be seen after the occurrence of a hanging man.

How to trade a hanging man?

As a hanging man is a bearish reversal candlestick pattern, one should look for shorting opportunities in a particular stock or index. Wait for the formation of the closing of the hanging man candle.

- Entry point: You can create a short position at the opening of the candle after the hanging man

- Confirmation: Look for a bearish signal, like a gap down or lower close, after a significant uptrend and hammer pattern is formed, to ensure reliability

- Stop loss: Place a stop loss above the high of the hanging man to limit potential losses if the trade goes against you.

In the above chart of Asian Paints, the entry would be at 3396, and the stop loss would be the high of the candle at 3398.

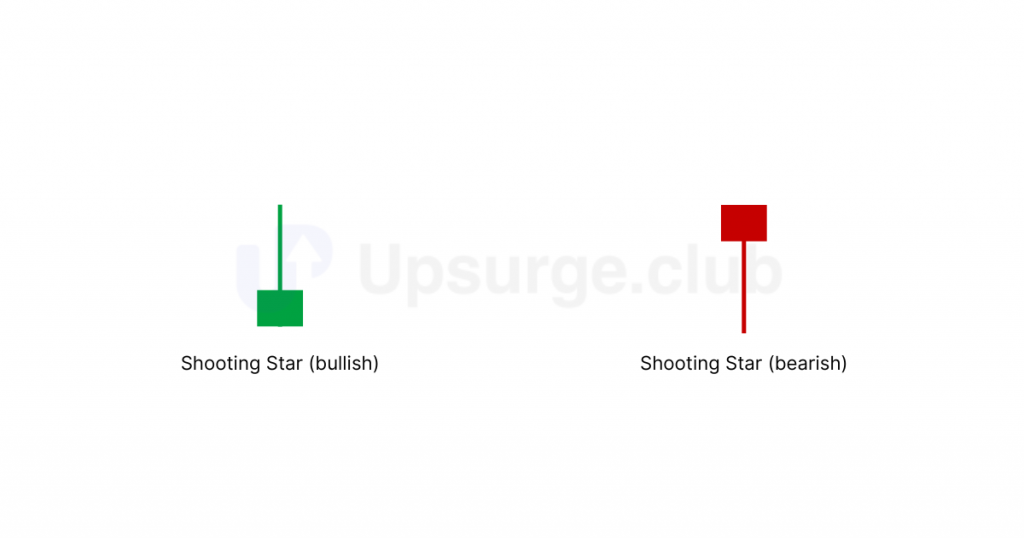

Shooting Star

How does a shooting star form?

The shooting star is a candlestick pattern, indicating potential trend reversal. It has a long upper shadow where the shadow length is at least twice the length of the natural body.

- The opening price is almost equal to the closing price,

- The low of the candle is nearly equal to the closing price, and

- There is a significant gap between the closing price and the high of the candle

Though the color of the candlestick does not change its interpretation, it is comforting to know when a shooting star is bearish. Here is how it looks:

Let’s look at the pattern forming in a chart:

Here’s the logic for the shooting star candlestick pattern formation. The stock is in an uptrend, with bulls in control, making new highs and higher lows. On the day the shooting star pattern forms, the stock trades higher and creates a new high.

However, selling pressure at the high point causes the price to drop, closing near the day’s low and forming a shooting star. This indicates the bears have entered, successfully pushing prices down, as evidenced by the long upper shadow. The bears are expected to continue selling in the coming sessions, potentially reversing the uptrend.

The longer the upper wick, the more bearish the pattern. According to the textbook definition, the shooting star should not have a lower shadow. However, as the chart above shows, a small lower shadow is acceptable. The shooting star is a bearish pattern; hence, the prior trend should be bullish.

Here is another example of a shooting star forming on the chart of Cipla Ltd.:

The highlighted candle has the following prices:

Open = 1167

High= 1185

Low=1167

Close=1173

The above candle qualifies as a shooting star since

- The prior trend is bullish

- The shadow-to-body ratio is 1.8 (~ 2)

How to trade a shooting star?

You should look for shorting opportunities when coming across shooting star candlestick patterns.

- Entry: Create a short position at the opening of the candle after the shooting star is formed

- Confirmation: A shooting star is confirmed if the next candlestick shows a lower close, indicating a potential bearish reversal.

- Stop loss: Place a stop loss at the high price of the shooting star candle to limit potential losses if the trade goes against you.

Inverted Hammer

How does an inverted hammer form?

The candlestick pattern is a shooting star formed at the bottom of a downtrend, signaling a bullish reversal.

An inverted hammer is formed when

- The opening price is almost equal to the closing price

- The low of the candle is nearly equal to the closing price, and

- There is a significant gap between the height of the candle and the close of the candle

Just like a hammer, the interpretation of this candlestick does not depend upon the candle’s color. But we have to look for a shadow-to-body ratio is double. This candlestick has a long upper shadow and no lower shadow.

The psychology of the inverted hammer shows a possible end to a downtrend, indicating that buyers are starting to take interest in the stock at lower prices. This means that after selling for a while, buyers step in and push the price up, forming a long upper shadow. Then, some selling happened again, bringing the price back near the opening level, creating a small body.

The below chart shows that Infosys’s inverted hammer took place at the end of the downtrend; after which the stock rallied significantly.

How to trade an inverted hammer?

An inverted hammer signifies an upcoming bullish trend. Here’s how a trade can be taken:

- Entry: Create a long position at the opening of the candle that forms after the inverted hammer.

- Confirmation: An inverted hammer is confirmed if the next candlestick shows a higher close, indicating a potential bullish reversal.

- Stop loss: Set a stop loss just below the low of the inverted hammer.

Let’s look at an example.

According to the rules, the trade setup for the above chart would be an entry at the closing of the inverted hammer at 398, and stop loss would be placed at the low of the candle at 392.

Target Setting for Single Candlestick Patterns

So far, we’ve explored the psychology behind single candlestick patterns and how to use them for entering trades. But have you ever thought about what our targets should be for these trades? Let’s dive into how we can set these targets strategically now.

To set a target, we need to know the risk-reward ratio concept.

The risk and reward ratio is a crucial concept in stock trading. It helps you understand how much you stand to gain compared to how much you might lose on each trade. This ratio can guide decisions to maximize profits and minimize losses.

Risk to Reward Ratio = Potential Gain / Potential Loss

If you buy a stock at a price of 100, and set a stop loss at 80, your potential loss (in case you hit the stop loss) is 20 (100 - 80). Similarly, if you set a target of 140, your potential gain (if you hit your target) is 40 (140 - 100).

Hence, the risk to reward ratio is 20:40, which can be written as 1:2.

We aim for a minimum risk-to-reward ratio of 1:1:5; let’s learn why.

Why Use the 1:1.5 Risk-to-Reward Ratio

The 1:1.5 risk-reward ratio means you aim to make 1.5 units of profit for every unit of risk. For example, if you risk ₹100 on a trade, your target profit is ₹150. This ensures your potential gains are more significant than your possible losses.

A key benefit is that it increases your chances of making a profit, even if not all trades are successful. With higher rewards for your risks, fewer winning trades can cover your losses and improve overall results. Setting a higher reward target keeps losses small compared to potential gains, which is crucial for long-term trading success. It helps you avoid significant losses that can impact your trading account.

Finally, the 1:1.5 risk-reward ratio offers a statistical advantage. Even if you win only 40% of your trades, this ratio can still lead to overall profits, making it an intelligent approach for trading in the volatile stock market.

Although it’s essential to choose a risk-reward ratio that matches your risk appetite, everyone’s comfort level with risk varies, so select a ratio that aligns with your individual trading goals and risk tolerance.

While knowing the 1:1.5 risk-reward ratio as a target is applicable, setting precise targets using a single candlestick pattern can be difficult. In the following chapters, we will discuss multiple candlestick patterns and indicators. These tools will help you set more effective targets and make better-informed trading decisions.

Let’s understand better with an example.

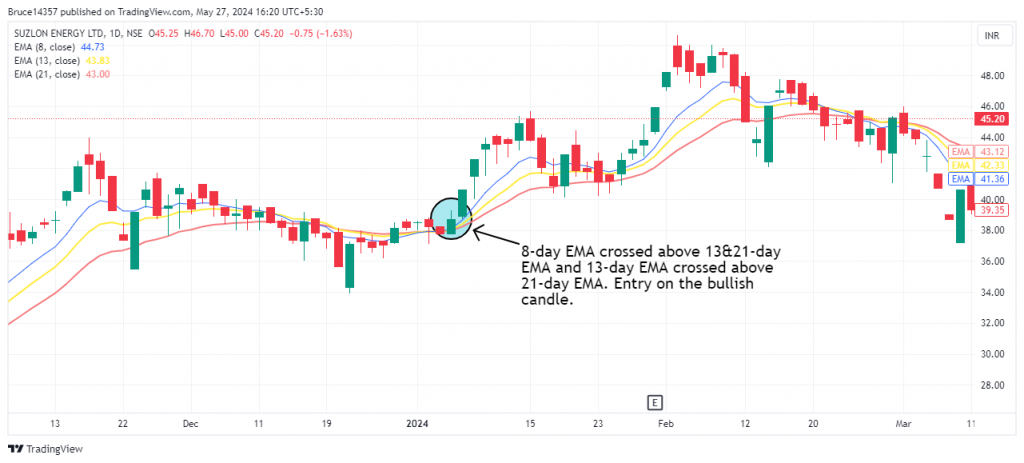

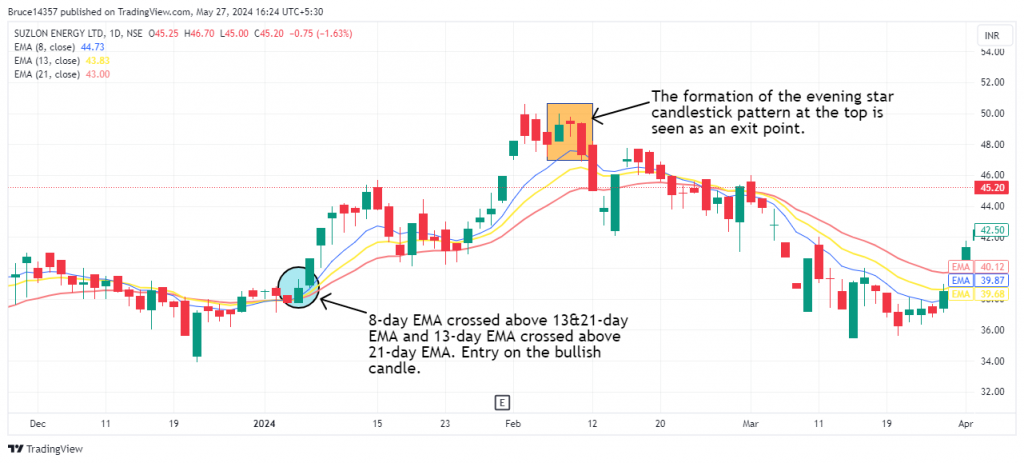

For instance, take Suzlon on a daily timeframe. It is forming a bearish marubozu angle candlestick. As we know, one should look for shorting opportunities because it signals bearishness. So we enter a short position at the closing of the candle, that is at 47.5, and we keep the stop loss at a high of the candle, which is at 52.40.

We now set a target of 40 so that Suzlon should go down by 7.5 points as our stop loss is approximately 4.5 points. In this way, we will have a risk of 5 in case it hits our stop loss and a reward of 6.8 points, maintaining the risk-to-reward of 1:1.5.

In the below image, you can see a short position on Suzlon’s stock, having a risk-to-reward ratio of 1:1.5:

Summary

- A hammer candlestick indicates a potential reversal from bearish to bullish sentiment. It is formed after a downtrend, with a small body at the upper end and a long lower shadow.

- The shooting star is a bearish candlestick that appears at the peak of an uptrend. It signals a potential bearish trend.

- The 1:1.5 risk-reward ratio helps ensure that your potential gains are greater than your losses, improving your trading results and protecting your capital.

- It’s difficult to set exact targets with single candlestick patterns alone, so we’ll examine more patterns and indicators for better accuracy.

Chapter 5: Two Candlestick Patterns

Two is better than one, even when it comes to candlestick patterns. In a double candlestick pattern, we analyze two candlesticks to make a trading decision. This means the trading opportunity unfolds over a minimum of two trading sessions.

This chapter will focus on some important two candlestick patterns: engulfing, harami, and tweezer candlestick patterns.

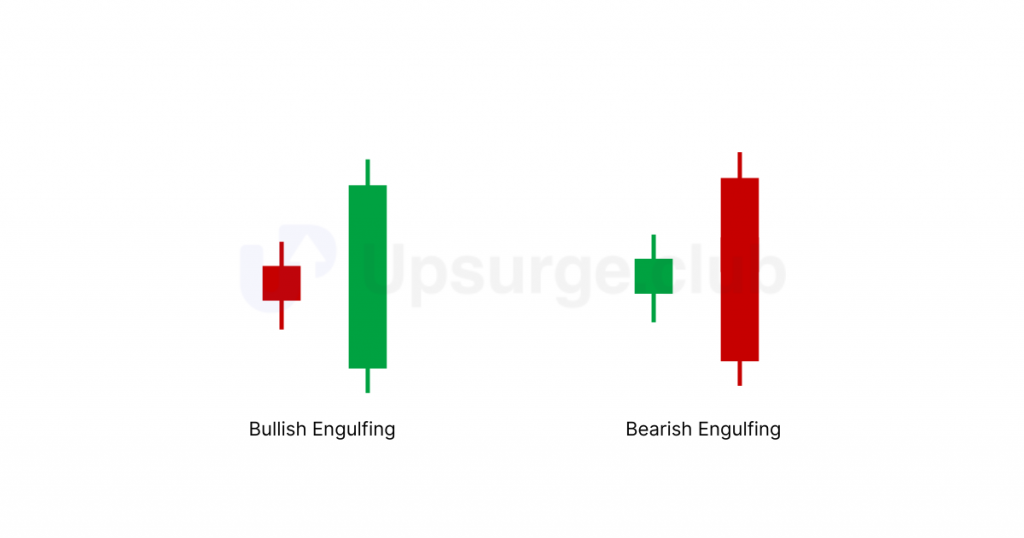

Engulfing Pattern

The first double candlestick pattern we are going to talk about is the engulfing pattern. As we have discussed earlier, double candlesticks require two candlesticks; the first candle with a relatively tiny body, and the second candle’s body completely engulfs the previous one and closes in the opposite direction of the trend. The engulfing pattern is a reversal pattern: it’s bullish at the end of a downtrend and bearish at the end of an uptrend.

Let’s look at their pictorial representation.

Bullish Engulfing Pattern

How does a bullish engulfing pattern form?

A bullish engulfing candlestick pattern occurs when it is found at the bottom of a downtrend. It is a potentially bullish reversal candle, which means that people tend to buy it after its formation.

The pre-requisites for a bullish engulfing candle are:

- The prior trend should be a downtrend.

- The first candle should be bearish, re-confirming the bearishness in the market.

- The second candle should be bullish, with a body long enough to engulf the whole previous candle, including its wicks.

Here is an image of a bullish engulfing candle forming at the bottom of a downtrend:

This is how it works:

- The market is in a downtrend, dominated by sellers, as shown by bearish (red) candles.

- A large bullish (green) candle forms, completely engulfing the previous bearish candle, signaling a solid shift in control to buyers.

- The bullish engulfing candle indicates strong buying interest and a change in market sentiment from bearish to bullish.

- This pattern suggests a potential reversal of the downtrend, with buyers gaining strength and the market moving upwards.

How to trade a bullish engulfing pattern?

Bullish engulfing is a potential bullish reversal trend that signals bullish sentiment in the market. The trading plan would be:

- Entry: Enter the trade at the opening price of the next candle, i.e., at the candle that forms just after the formation of the engulfing candle.

- Confirmation: An entry is confirmed if it is found after a downtrend, the second candlestick is bullish and engulfs the previous bearish candle, and the candlestick formed after the pattern closes higher than the bullish candle’s high, indicating a potential bullish reversal.

- Stop loss: Place the stop loss just below the low of the bullish engulfing pattern. This helps to minimize risk in case the pattern fails.

You must remember how to set a target, as explained at the end of the single candlestick chapter. If you need a refresher, give it a quick read here. The same applies to 2 candlestick patterns, too.

Assuming we are going long on Tata Motors, where a bullish engulfing pattern is formed.

- Entry for the above bullish engulfing candle is the opening of the following candle, which is at 122.80.

- Stop loss would be low of the previous candle, which would be at 113.00.

- The target is to aim for a risk-to-reward ratio of 1:1.5.

There often needs to be more clarity about whether a bullish engulfing pattern needs to engulf the entire previous candle, including the wicks, or just the natural body. If the natural body is engulfed, it can be considered a bullish engulfing pattern. Some may disagree, but what truly matters is how effectively you develop your trading skills with this pattern.

Bearish Engulfing Pattern

How does a bearish engulfing pattern form?

A bearish engulfing pattern signals bearishness in the market and indicates a potential reversal from an uptrend to a downtrend. It forms during an uptrend and suggests that the market sentiment has shifted, opening the door for a downward move.

The pre-requisites for a bearish engulfing candle are:

- The prior trend should be an uptrend.

- The first candle should be bullish, reconfirming the bullishness in the market.

- The second candle should be bearish, and long enough to engulf the green candle.

Here is a chart that has a bearish engulfing pattern forming at the end of an uptrend:

The above chart shows a bearish candle formed after an uptrend, totally covering the previous bullish (green) candle. There is a significant drop in the market after the occurrence of a bearish engulfing pattern.

- The market is in an uptrend, dominated by buyers, as shown by bullish (green) candles.

- A significant bearish (red) candle forms, completely engulfing the previous bullish candle, signaling a solid shift in control to sellers.

- The bearish engulfing pattern indicates intense selling pressure and a change in market sentiment from bullish to bearish.

- This pattern suggests a potential reversal of the uptrend, with sellers gaining strength and the market moving downwards.

Now, let’s see how we should trade the bearish engulfing pattern.

How to trade a bearish engulfing pattern?

- Entry: Enter the trade at the opening price of the next candle, i.e., at the candle that forms just after the formation of the engulfing candle.

- Confirmation: A bearish engulfing pattern is confirmed if it occurs after an uptrend, the bearish candle completely engulfs the previous bullish candle, and the next candle closes lower than the low of the bearish engulfing candle, signaling a potential bearish reversal.

- Stop Loss: Set the stop loss at the high of the bearish engulfing candle to minimize risk if the pattern fails.

Let’s look at how a trade in Ashok Leyland enflolds using the bearish engulfing candlestick pattern.

- Entry: Enter the trade at the opening of the next candle, which is 176.40.

- Stop Loss: Set the stop loss at the high of the bearish engulfing candle, which is 177.00.

- Target: Aim for a target with a risk-to-reward ratio of 1:1.5 based on the entry price.

Harami Pattern

Harami’ in Japanese means ‘pregnant’. Being a two-candlestick pattern, the first candle is significant and reflects strong market sentiment, either bullish or bearish, depending on the current trend. The second candle is smaller and has its body completely engulfed within the first candle’s body, indicating a potential reversal in the trend.

The below image shows a harami candlestick pattern.

Here, you can see that the previous candle completely covers the second candle. Now, let’s talk about both harami candlestick patterns – bullish harami and bearish harami.

Bullish Harami Pattern

How does a bullish harami pattern form?

The harami pattern is a potential reversal signal that signifies a change in market sentiment.

The pre-requisites for a bullish harami pattern are:

- The prior trend should be a downtrend.

- The first candle should be bearish, confirming the bearishness in the market.

- The second candle should be bullish and small, fitting within the body of the first red candle.

Here is the formation of a bullish harami candlestick pattern, forming at the bottom of a downtrend.

The psychology behind a bullish harami candlestick pattern is:

- Initially, the market was in a downtrend, dominated by sellers, which was reflected by the large bearish (red) candle.

- The sizeable bearish candle confirms the ongoing bearish sentiment in the market.

- The following day, a smaller bullish (green) candle forms within the body of the previous red candle.

- This smaller candle represents a period of indecision (doji candles can be formed here) where the selling pressure has weakened, and buyers are starting to enter the market.

- The green candle’s appearance suggests buyers are becoming more active, although their presence is not strong enough to reverse the trend completely.

- The pattern indicates that the downtrend might be losing its momentum. If buyers continue to gain strength, a reversal from bearish to bullish could be on the horizon.

How to trade a bullish harami pattern?

With an understanding of the bullish harami candlestick pattern, let’s talk about trading it. This pattern suggests a bullish reversal, so look for buying opportunities in the stock.

- Entry: Buy when the price moves above the high of the second (green) candle.

- Confirmation: For added assurance, wait for the next candle (third candle) to close higher than the high of the first (bearish) candle.

- Stop loss: Place the stop loss just at the low of the second (green) candle to protect yourself if the pattern doesn’t work out.

Let’s look at an example in Tata Motors.

The OHLC data of the above candlesticks are:

First candle:

Open = 414.50

High = 414.50

Low = 400.40

Close = 409.20

Second candle:

Open = 401.60

High = 410.60

Low = 401.40

Close = 409.60

You can see that the first candlestick does not entirely cover the low of the second candle. But remember that we need to be flexible!

Hence, here’s how we would trade:

Entry Point: 410.60

Stop Loss: 401.40

To gain more confidence in the bullish harami pattern, watch for the third candle. For a more decisive confirmation, the third candle should be bullish. You can initiate a trade setup if the third candle closes above the high of the first candle, i.e., above 414.50. Set your stop loss at the low of the first candle.

Now, let’s look at the bearish harami pattern, which works just the opposite of the bullish harami pattern.

Bearish Harami Pattern

How does a bearish harami pattern form?

It is a potential bearish reversal candle, and the pre-requisites for a bearish harami candlestick pattern are:

- The prior trend should be an uptrend.

- The first candle should be bullish, indicating bullishness in the market.

- The second candle should be bearish and small enough to be contained within the body of the first candle.

The psychology behind the formation of bearish harami candlesticks is as follows:

- The market is in an uptrend, dominated by buyers.

- A large bullish (green) candle confirms the ongoing bullish sentiment.

- The following day, a smaller bearish (red) candle forms within the body of the previous green candle.

- This smaller red candle represents a period of indecision (Doji candles can form here), indicating that the buying pressure has weakened and sellers are starting to enter the market.

- The new small bearish candle suggests that sellers are becoming more active, though their presence still needs to be more robust to reverse the trend completely.

- The pattern indicates that the uptrend might be losing momentum.

- If sellers continue to gain strength, a reversal from bullish to bearish could be on the horizon.

The image of a bearish harami, seen forming at the top of an uptrend in the price chart of Infosys:

How to trade a bearish harami pattern?

- Entry: Sell when the price moves below the low of the second (red) harami candle.

- Confirmation: For added assurance, wait for the next candle (third candle) to close lower than the low of the first (bullish) candle.

- Stop Loss: Place the stop loss at the high of the second (red) harami candle to protect yourself if the pattern doesn’t work out.

Now, let’s look at another exciting double candlestick pattern!

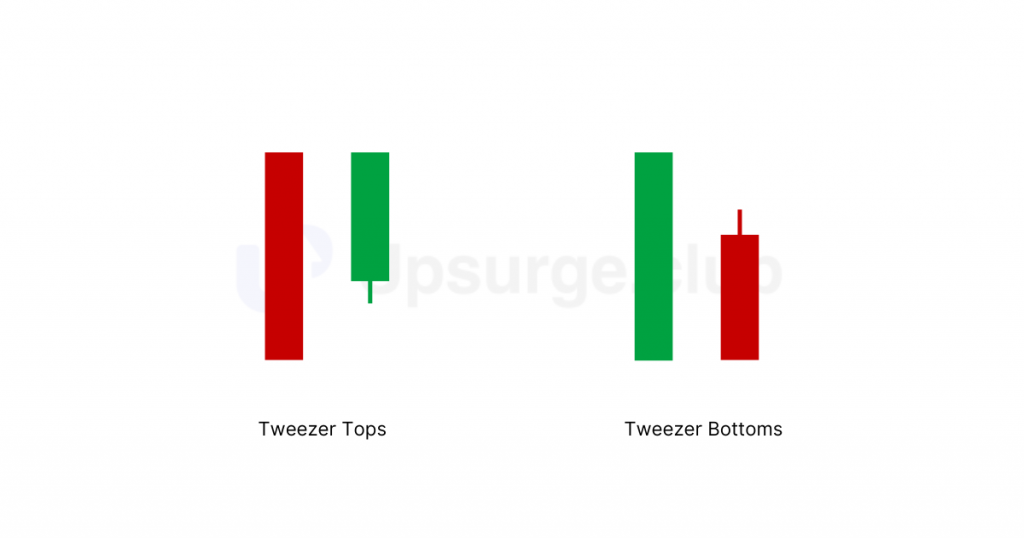

Tweezer Tops and Tweezer Bottoms

These consist of two consecutive candles with matching highs (tweezer top) or matching lows (tweezer bottom). Here’s how they look:

Let’s take a closer look at each one of them.

Tweezer Bottoms Pattern

How is a tweezer bottom formed?

It is a potential bullish reversal pattern, called a tweezer bottom, because it is found after a downtrend. The pre-requisites for a tweezer bottom candlestick pattern are:

- The prior trend should be a downtrend.

- The first candle should be bearish (red), confirming the bearishness in the market.

- The second candle should be bullish, and have a low that matches or is very close to the low of the first red candle.

Let’s examine the tweezer bottom pattern, which forms at the bottom of a downtrend of Infosys stock, for a better understanding.

As you can see in the above chart, Infosys stock rallied significantly after the formation of the tweezer bottom. This pattern, formed after a downtrend with both candles having similar lows, indicates a potential bullish reversal.

What does the tweezer bottom tell us?

- Initially, the market was in a downtrend, dominated by sellers, as shown by the large bearish (red) candle. This sizeable bearish candle confirms the ongoing negative sentiment in the market.

- The next day, a bullish (green) candle forms with a low that matches or is very close to the low of the previous red candle. This matching low suggests that the selling pressure is weakening, and buyers are starting to step in.

- The green candle’s appearance indicates buyers are becoming more active, although their presence still needs to be stronger to reverse the trend completely.

- This pattern signals that the downtrend might be losing its momentum if buyers continue to gain strength.

Let’s look at how to trade tweezer bottom.

How to trade a tweezer bottom?

Now that you understand the tweezer bottom candlestick pattern, let’s discuss how to trade it. This pattern shows a potential bullish reversal, so it’s a good time to look for buying opportunities in the stock.

- Entry: Buy when the price moves above the high of the second (green) candle.

- Confirmation: Make sure the next (third) candle closes higher than the high of the second (green) candle to confirm the reversal.

- Stop Loss: Place the stop loss just below the low of the second (green) candle to protect yourself if the pattern doesn’t work out.

Now, let’s discover the tweezer top double candlestick pattern.

Tweezer Tops Pattern

How does a tweezer top get formed?

Converse to a tweezer bottom, a tweezer top is formed after an uptrend. The pre-requisites for the formation of a tweezer top are:

- The prior trend should be an uptrend.

- The first candle should be bullish, confirming the bullishness in the market.

- The second candle should be bearish, and have a high that matches or is very close to the high of the first candle.

Let’s understand with an example.

In the above chart, you can see they are formed in an uptrend; the OHLC of the above candlesticks are:

First candle:

Open = 1553

High = 1575

Low =1547

Close =1573

Second candle:

Open = 1572

High = 1572

Low =1545

Close =1553

We can see the high prices of both candles match, confirming the tweezer top candlestick pattern.

The psychology behind the formation of the tweezer top is as follows:

- Initially, the market was in a downtrend, dominated by sellers, shown by a large bearish (red) candle.

- The next day, a bullish (green) candle forms with a low matching or very close to the previous red candle’s low, indicating weakening selling pressure.

- This matching low suggests that buyers are starting to step in, though not yet strong enough to reverse the trend completely.

- The pattern signals that the downtrend might be losing momentum.

If buyers continue to gain strength, a reversal from bullish to bearish could be on the horizon.

How to trade a tweezer top?

- Entry: Sell when the price moves below the low of the second (red) candle.

- Confirmation: Make sure the next candle closes lower than the low of the second (red) candle to confirm the reversal.

- Stop Loss: To protect yourself if the pattern doesn’t work out, place the stop loss at the high of the second (red) candle.

Now that you’ve got the hang of interpreting and trading single and two-candlestick patterns, let’s move on to multi-candlestick patterns.

Chapter 6: Multiple Candlestick Patterns

Continuing from the previous chapter on double candlesticks, where we discussed engulfing, harami, and other patterns that help us enter the market, we now move on to multiple candlestick patterns. These patterns involve analyzing three or more candlesticks, but we will focus on just three candlesticks to understand the market direction better.

You might wonder why it is necessary to analyze three candlesticks. The reason is simple: the more candlesticks, the more solid and reliable the trend.

In this chapter, we will explore patterns like morning and evening stars, three black crows and soldiers, three inside up and down, and three rising and falling methods. These patterns give us a clearer picture of the market and help us make better trading decisions.

Let’s look at the first multiple candlestick pattern, the morning star.

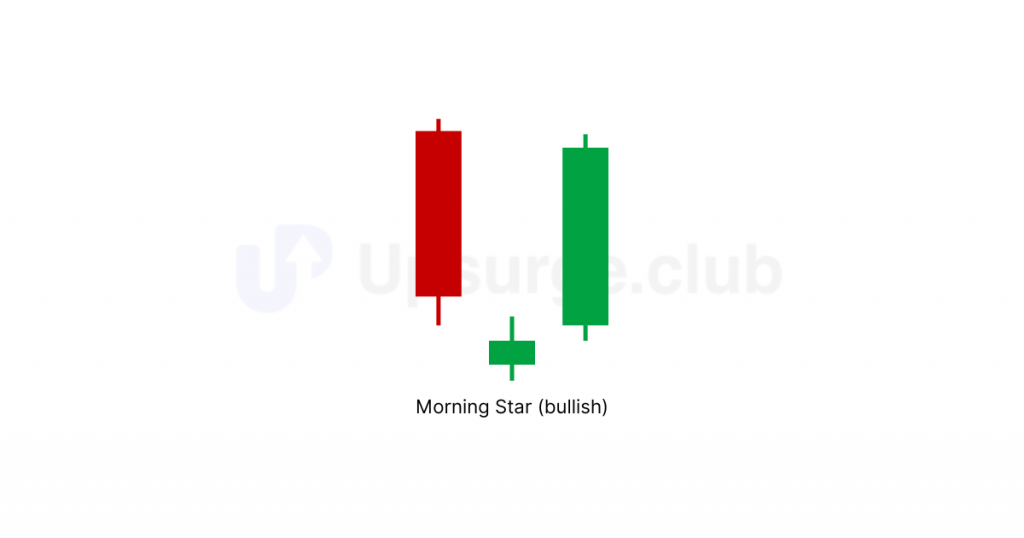

Morning Star

How is a morning star pattern formed?

A bullish candlestick pattern generally formed at the bottom of a downtrend, the morning star consists of three candlesticks.

To improve our understanding, we will denote the first candle as C1, the second candle as C2, the third candle as C3, and so on.

- The first candle (C1) is bearish, with the closing price near the previous candle’s low.

- The second candle (C2) is a doji, having a negligible body. It should form below the low of the first candle

- The third candle (C3) should be bullish and close higher than the high of the first candle (C1), like a bullish engulfing candle.

Here’s a pictorial representation of the same:

Let’s break down the same.

- The market is in a downtrend, with the bears in control, forming successive new lows.

- On day 1 (C1), the market forms a long red candle, showing selling acceleration.

- On day 2 (C2), the market forms a doji or spinning top, indicating indecision and causing restlessness among the bears who expected another down day.

- On day 3 (C3), a green candle forms, closing above C1’s red candle opening.

Buying persists throughout C3, recovering all losses of C1. - The bullishness on C3 will likely continue, suggesting buying opportunities in the market.

How to trade a morning star pattern?

The three characteristics of a morning star are found in the HDFC Bank chart below.

Here’s how to trade it.

- Entry: Enter a long position at the candle’s opening that forms after the morning star pattern.

- Confirmation: A morning star is more reliable in a downtrend if C3 (the green candle) closes above the midpoint of C1 (the red candle), indicating a potential bullish reversal.

- Stop Loss: Place a stop loss at the low of C2 (the doji) to limit potential losses if the trade goes against you.

Let’s now move on to the evening star.

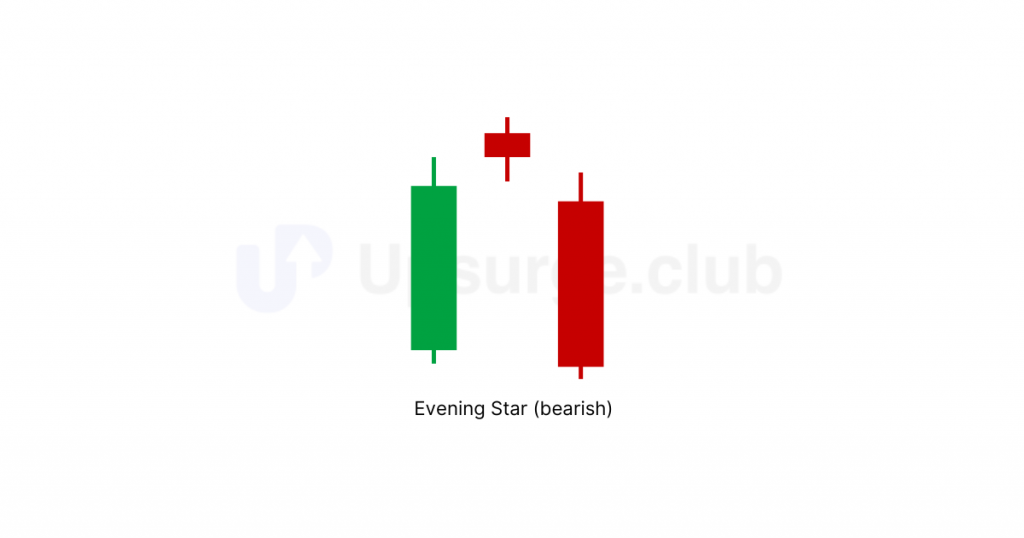

Evening Star

How is an evening star pattern formed?

This candlestick pattern signifies a potential bearish reversal, often forming at the end of an uptrend. It indicates that buyers have lost control and bears have made their entry. It also consists of 3 candlesticks.

Here’s how it is constructed:

- The first candle (C1) is bullish, with the closing price near the previous candle’s high.

- The second candle (C2) is a doji with a negligible body, indicating indecision. This forms above C1.

- The third candle (C3) is bearish and closes lower than the first candle (C1), similar to a bearish engulfing candle.

Here is a pictorial representation of the same: