Chapter 5: Going With the Cash Flow

So far, we have seen how a company earns a profit. But how much of this profit converts into cash? In this chapter, we will understand the concept of accrual accounting and how a cash flow statement tells you about a company’s financial health.

As the saying goes, behind every hard-working profit & loss statement is a smart working cash flow statement.

The profit & loss statement shows you all the work the company did. What it doesn’t tell you is whether the company received cash for the work it did. Work completed and billed is what is called ‘accrued revenue.’ To put it in layman’s terms, you sure have earned it, but have you been paid for it? That is the question.

While the P&L plays the hero onscreen, it has a sidekick who works behind the scenes and makes the P&L happen smoothly – the cash flow statement.

Why do you need a cash flow statement? Why can’t P&L just account for sales for which you received cash?

Because you have to give credit to the customer many times, every customer won’t buy a car on a full down payment. Electricity and gas bills are calculated after you have used the service. In all these instances, the business accrues revenue, and the customer pays later.

Now, you may wonder, but why report accrued revenue in the first place? Why not just account for sales for which you received cash? Because business doesn’t work that way.

Why does one report accrued revenue and not cash revenue?

Remember, the objective of a P&L statement is to calculate the profit/loss earned from your business operations. If you run a lemonade stand, you should know whether selling lemonade earns you any money or you are just losing money.

Let’s take a hypothetical scenario.

You run a lemonade stand and sell one glass of lemonade for ₹10. The cost incurred to make one glass is ₹4. Your profit is ₹6. That’s what the P&L statement tells you. Now, Jay walks in and gives you the order to deliver ten lemonades every day for 30 days and collect the money (₹3,000 = ₹100 x 30 days) at the end of the month. Here, you accrue ₹100 every day in revenue as you bear the cost of the ingredients or raw materials used to make the lemonade, such as lemon sugar, water, ice, and spices.

Since you have accounted for the revenue but have not received the cash, it piles up into a separate heading called “Accounts Receivables.”

Pay close attention to this “Accounts Receivables” as it plays a major role in the climax. Many scams take place in this segment.

When Jay’s Accounts Receivable (AR) reaches ₹3,000, he pays you, and your account with Jay is settled. You will report this cash as accounts receivable in your cash flow statement.

If Jay doesn’t pay the amount for three months, your AR keeps growing. But your P&L shows a profit of ₹1,800 (₹6 x 10 glasses x 30 days) per month despite not getting paid for it. It means a company can be profitable and still be low on cash as its cash is stuck in transit. You can sustain for one month or two months. But if the credit keeps growing and Jay doesn’t pay, it will affect your operations because you are bearing the cost of ₹1,200 (₹4 x 10 glasses x 30 days) per month to make those 300 glasses of lemonade.

Do you see why P&L needs a cash flow (CF) statement? Because it gives you the real picture of how much cash you are getting.

The cash flow statement plays a very important role in maintaining the finances of a company. If P&L are the muscles, cash flow is the oxygen. Hence, when cash flow reduces, your business operations get affected.

Even a profitable company can be burning cash. And even a loss-making company can have bundles of cash. To do this, you need to read the cash flow statement thoroughly.

Bird’s eye view of the cash flow statement

To read this statement, we need to understand how cash flows into the business.

Going back to our lemonade example.

The P&L brother wants to buy a bike worth ₹1 lakh to deliver lemonades. In what ways can he fund his bike?

Take a loan from the bank or family – Cash Flow From Financing or CFF

Use the cash he earned from selling lemonades – Cash Flow From Operations or CFO

Invest the operating cash in fixed deposits, stocks, and mutual funds and use the accumulated money to buy a bike – Cash Flow from Investing or CFI

Each method involves costs and tells you something about the lemonade stand.

Assuming you take a loan to buy a bike. Your lemonade stand’s cash flow statement will look something like this.

Sr. no | Particulars | Amount (₹) | Notes |

1 | Cash Flow from Operations |

|

|

| Profit | 5400 | You start with the Profit |

| Accounts Receivables | (9000) | Since you did not receive the cash, it will be deducted from your cash balance until Jay clears his dues. |

| Net Cash from Operations | -3600 |

|

2 | Cash Flow from Investing |

|

|

| Purchase of Bike | (1,00,000) |

|

| Net Cash from Investing | (1,00,000) |

|

3 | Cash Flow from Financing |

|

|

| Loan | 1,00,000 |

|

| Interest and Processing Fees | (1000) |

|

| Net Cash from Financing | 99,000 |

|

The above table is just a framework of a cash flow statement. It has other elements like net cash balance, which we will study later in the chapter.

In an ideal scenario, you would want your lemonade sales to earn you enough cash to cover your expenses and pay for the bike. The bike is an investment as it will allow you to sell more and earn more revenue and profit.

That’s how money makes money.

So far, we have seen a scenario where you sell 300 glasses of lemonade a month. Now imagine this business in lakhs and crores, with lemonade selling in huge volumes nationally and internationally. Imagine what the gap between the P&L statement and cash flow statement would look like then!

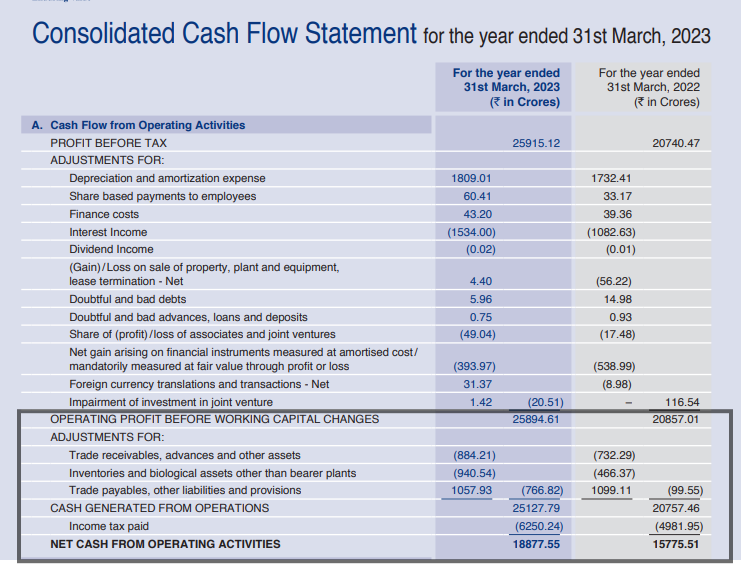

On a larger scale, the cash flow statement becomes even more important as your operations have to earn you enough cash for the business to sustain. Let’s read the cash flow statement of a real bigwig like ITC and see what it tells you.

What does operating cash flow tell you?

We will not get into the nitty-gritty of calculating operating cash flow. Remember, we are here to only read the statement, not make it.

Between the line “Profit before tax” and the line “Operating profit before working capital changes,” the company has deducted all non-operating expenses (which we discussed in the previous chapter).

Note: “()” indicates that the cash has gone out of the business and is reducing your cash balance. When reading the cash flow statement, put yourself in the company’s shoes and follow the cash trail, whether it is coming in or going out.

Our cash flow from operations begins with “Operating profit before working capital changes.”

- ITC’s trade receivables increased to ₹884.21 crores in FY23 from ₹732.29 crores in FY22.

- Inventories are the amount ITC pays to store the supplies for business operations. Its inventory cost more than doubled to ₹940.54 crore.

- Trade payable is the amount ITC has yet to pay its suppliers. Since the cash has not left the business, this amount is positive. It is relatively flat compared to FY22.

In ITC’s case, it converted ₹25,894 crore profit into cash, which is much higher than its accounts receivables and inventories. It shows that the company’s operations are generating healthy positive cash flows to fund any credit sales and invest in the business.

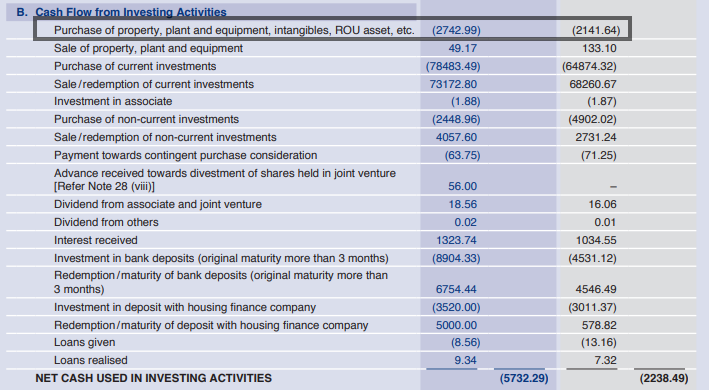

What does investing cash flow tell you?

The word investing has to be taken in its literal sense. In our lemonade example, you purchased a bike as an investment to earn more money from deliveries. The purchase of any capital goods like property, equipment, and vehicles that will earn you income for a long time is considered an investment.

The above cash flow from investing activities is self-explanatory. Like you, even big companies invest surplus cash to earn dividends and interest.

However, the crux of this segment is to see how much the company is reinvesting in its business for expansion, acquisition, or any other activity that could help it earn more money because you are investing in ITC for the cash it earns from FMCG, hotel, agriculture, and paperboard business.

ITC spent ₹2,743 crore in the purchase of capital goods like plant, equipment, and property. This shows how the company is using its cash. If a company is acquiring another business, its investing cash flow will suddenly shoot up.

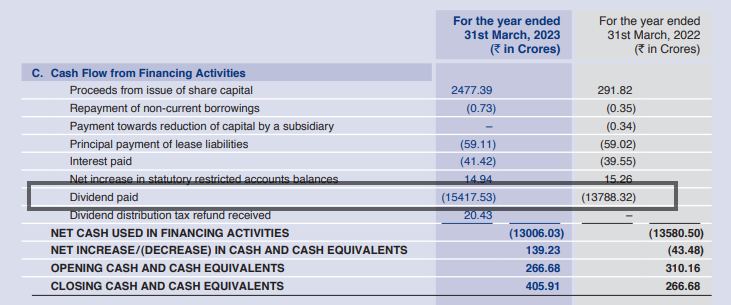

What does financing cash flow tell you?

The most crucial part of the cash flow statement for an investor is the financing cash flow. It shows you how much of the company’s cash is coming in or going out in debt and equity.

In our lemonade example, we saw that you funded the bike by taking a bank loan. When the loan passed, there was a significant cash inflow from financing activities as cash came into the business. However, the interest and principal paid on this loan will result in a cash outflow from financing activity.

In ITC’s case, you can see that the company spent ₹15,417 crore in paying dividends to shareholders in FY23 compared to ₹13,788 crore last year. This will also be considered as a cash outflow.

What does the cash flow statement tell you about the company?

All three elements combine to tell you whether your overall business increased or decreased your cash balance. That is where you get a positive cash flow or negative cash flow.

Here is ITC’s FY23 cash flow snapshot:

Particulars | Amount (₹ crore) |

Net Cash from Operations | 18,877.55 |

Net Cash from Investing | -5,732.29 |

Net Cash from Financing | -13,006.03 |

Net Cash Increase/(Decrease) | 139.23 |

This means that in FY23, ITC increased its cash balance by ₹139.23 crore. The majority of its cash came from operations, which it used for investing and financing activities (majorly dividend payments).

ITC opened FY23 with a cash balance of ₹266.678 crore (which is the same as the closing balance of FY22). Its FY23 business activities increased its cash balance by ₹139.32 crore to ₹405.9 crore.

This was for ITC’s cash flow statement in a strong market. A company has to balance how much cash to keep and how much to use. If the market is uncertain, companies hoard more cash to keep cash flowing in the business.

(i) Phase of the business cycle

A cash flow can tell you a lot about which phase the business is in. We will go back to chapter 2 where we discussed the business phases.

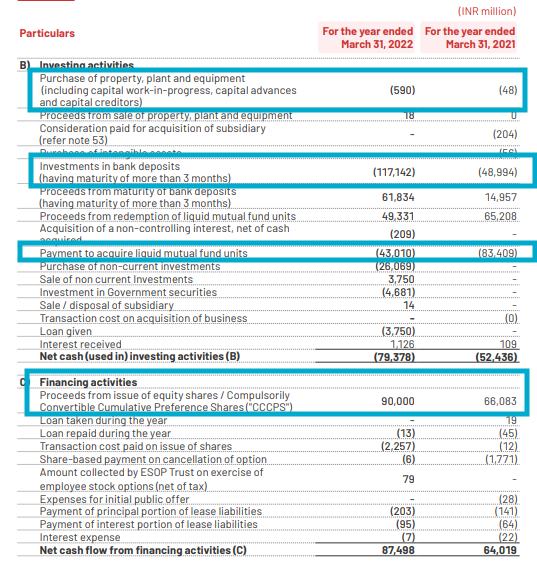

A startup or company in the early stages of growth is likely to have negative cash flow from operations. Their investing cash flow is high as they reinvest the money to grow the business operations. If a company launches an IPO, its financing cash flow will be high.

Take Zomato, for instance. Zomato launched its IPO in July 2021. If you look at its cash flow from financing activities, there is a ₹90,000 million cash inflow from proceeds from equity shares. In the short term, it parked its IPO proceeds in bank deposits and liquid mutual funds and reinvested ₹590 million in the business.

On the other hand, a company in a mature stage will have high operating cash flow and low investing and financing cash flow, as in the case of ITC.

A company’s cash flow statement is much like an individual’s financial health – a person who recently started a job (only one source of income) versus a person at the peak of his/her career with multiple sources of income (salary, investments, side hustle).

But this is only one side of the coin.

(ii) Positive vs. negative net cash flow

Remember how we said that a profitable company could have negative cash flow and a loss-making company could have positive cash flow?

Throughout the year, adding up the operating, investing, and financing activities could either give positive or negative net cash flow, which is reflected in the cash flow statement.

And just like in literature, even in business, all that glitters is not gold.

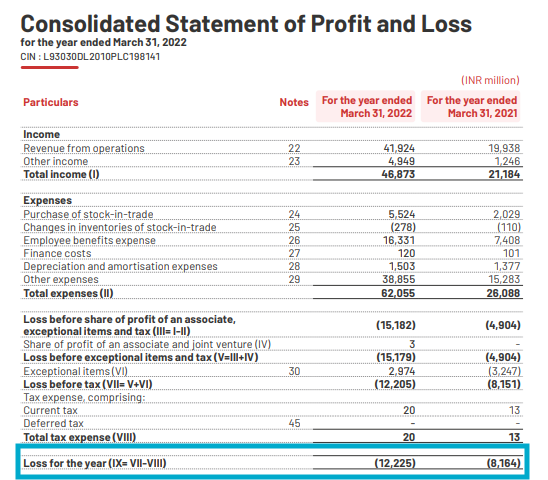

Loss-making company with positive cash flow: In the above example of Zomato, it has a positive net cash balance of ₹1,190 million. But the company has been making losses. It reported a net loss of ₹12,225 million in FY22.

A company could also have a positive cash flow if it sold some assets like land, property, and a business segment. There will be positive investing cash, but this method needs to be more sustainable.

A profitable company with negative cash flow: A profitable company can also report negative cash flow if it has made a major investment, such as buying a plant or machinery or a major acquisition. Think of it this way: Ananya, a salaried employee earning ₹12 lakh per annum (Operating cash flow), buys a ₹1.5 crore house (Investing cash flow). So, her cash flow will be negative for that year. But that doesn’t affect her operating cash flow or her profits.

In today’s Buy Now, Pay Later world, the cash flow statement has become an ever more critical fundamental analysis.

When you look at the role our cash flow sidekick plays, it supports the P&L by providing finance from debt and equity and investing it in plant and machinery. In return, the P&L earns more cash from operations and thus continues the cycle.

Next up: The curious case of the Balance Sheet.

Summary

- A P&L statement tells you how much business a company did (billed their clients for services or sales) and how much profit/loss it made from this activity. This is called ‘accrued earnings’.

- The cash flow statement records the cash inflow and outflow of every transaction.

- If a client did not pay for a service, it is recorded in Accounts Receivables and deducted from a company’s profits. Until the client pays for the service, it comes out of the company’s pockets and reduces its cash balance.

- A cash flow statement is divided into three elements based on the source of cash. A business raises finance (debt, equity) to commence operations (cash flow from financing). It then invests in business to buy plant and equipment (cash flow from investing). Once the operations begin, cash is earned from the company (cash flow from operations).

- Each cash flow element talks a lot about a company’s growth phase.

- A startup may have negative operating cash flow as it is making losses.

- A growth-stage company may have high negative investing cash flow as it is reinvesting the money in expansion.

- A mature company may have a high positive operating cash flow and low negative investing and financing cash flow.

- All three elements tell you whether your overall business increased or decreased your cash balance. Add up the net cash from operations, investing, and financing, and you will either have a positive or negative net cash flow.

- A loss-making company can have positive cash flow if it raises money in an IPO or sells its land or business for cash.

- A profit-making company can have negative cash flow if it invests significantly in expansion, such as a new plant or acquisition.