Chapter 6: Finding Balance with the Balance Sheet

In this module, we will learn how the balance sheet takes inputs from the profit & loss account and cash flow statement and presents the overall financial report of a company. We will dive deeper into each segment of the Balance Sheet and what it infers to help you make informed decisions.

We are halfway through the journey of fundamental analysis. We have understood how to look at a company from the lens of a fundamental investor, skimming through its business model, annual report, and business operations.

While you should track the daily business routine, the company’s true worth is known from its balance sheet.

To put it in the Bollywood language,

In the movie Deewar, Amitabh Bachan says, ”Aaj mere paas bangla hai, gaadi hai, bank balance hai (Tangible assets),” and Shashi Kapoor replies, “.. mere paas maa hai (Intangible asset).”

This one statement doesn’t tell you how much they earn, but how much net worth is.

And that is what the balance sheet is all about.

The balance in ‘balance sheet’

Let’s say you have to calculate your net worth. You will list down all your financial achievements from the day you started earning. It includes everything you purchased under your name (clothes, jewelry, house, car, mutual funds, stocks) and how you financed your purchases from Day 1 of your earnings.

Going back to our lemonade example in the previous chapter, you can buy a bike either from your OWN money (your savings, money from family, payments you get from selling lemonade) or OWED money (loan from banks or creditors).

💡Remember that Assets = Liabilities + Equity

Hence, a balance sheet,

- is a sheet listing down everything you own as assets and everything you owe as liabilities since you are liable to pay it in the near or far future.

- should be balanced, meaning every asset you own should have a source of funding (Owner’s money or borrowed money). If the sheet doesn’t balance, it raises suspicion about where you got the money to buy the asset.

Note: The company is a separate legal entity. If you, the business owner, put your money into the business, the company is liable to pay you interest/returns for the money you invested. Hence, the owner’s money is owed money in the company’s balance sheet and is recorded under the head “Shareholders Equity.”

What does a balance sheet tell you?

Who and why would someone be interested in knowing your assets and liabilities?

- Who – the business owners (shareholders), creditors, suppliers, investors, customers, and any other party with financial interest in your company.

- Why – to know where the company is using the capital and if it can pay its bills and loans while making money for the owner (dividends etc).

Capital

In this context, capital is the money used for productive or investment purposes. When a business invests money to generate revenue/income or buy equipment that will help in generating revenue/income, that money is called capital.

A business is like a transaction. You always want your money’s worth and, if possible, something extra. Let’s take a daily life example. You purchase a mobile worth ₹1.5 lakh. Note that the sentence states “worth”. You know it’s basically the features and services for which you are paying ₹1.5 lakh. And you would be happy if you get something extra like an extended warranty or a 3-month subscription.

Loans and Investments are also transactions. When you give a loan to someone, you want to know where they are using the money and if they can repay the money with interest. When you invest in a company you should seek information on how they plan to use the money and if they can return you more than what you invested over a long term. This information can be obtained from the balance sheet.

Reading a balance sheet

The balance sheet begins with the business owner’s fund which they use to buy inventory and earn revenue. As the business expands, they raise capital from debt/equity to purchase assets and earn more income. This cycle continues and increases/ decreases the value of a business.

Let’s look at a balance sheet’s 3 segments:

- Shareholder’s equity

- Liabilities

- Assets

We will take each part of the balance sheet and then join them to see how all 3 balance to make a complete balance sheet.

(i) Shareholder’s equity

Every business is self-funded at the start. The owner divides his/her ownership into shares (with a face value of ₹10) and sells them to investors to raise equity capital. When you buy equity shares of a company, you become part owner and share both the company’s profits and losses.

You might wonder why shares with a face value (FV) of ₹10 are listed on the stock exchange at different prices. That is where the shareholder’s equity comes in.

All companies start at the same price point ₹10/share. Over the years, the business operations create value through profits/losses which changes the value of the stock. If a company splits a stock, the FV reduces.

Below is the shareholder equity of Eicher Motors:

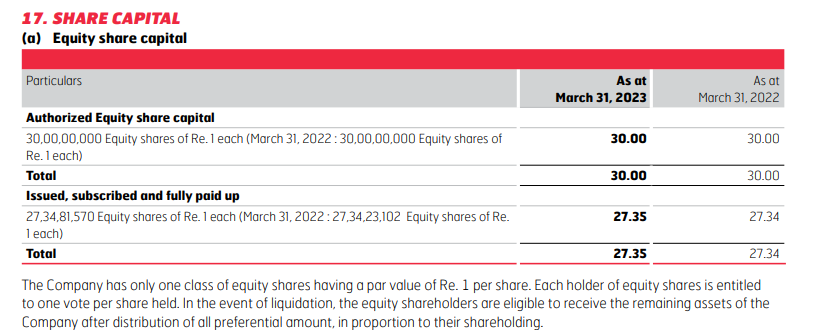

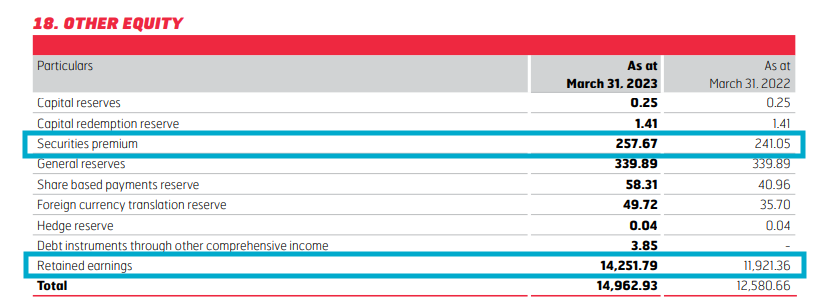

If you look carefully, there are two segments: “Equity share capital,” which is the face value of shares, and “Other equity,” which is the value the company created through its business. Let’s look at the details in Notes 17 and 18.

Eicher Motors has divided its ownership into 30 crore equity shares with FV of ₹1. However, it has only issued 27,34,81,570 shares so far. It can issue the balance shares as and when it needs more capital. The FV of Eicher Motor shares is ₹1/- as the company did a 1:10 stock split in February 2023. For every 1 share of Eicher Motors, shareholders got 10 shares, which reduced its FV from ₹10 to ₹1.

Note: A company does a stock split if its trading value on the stock exchange increases, making it difficult for retail investors to buy shares.

The value of “other equity” is higher as it shows the value the company generated over the years.

Line 3 – Securities Premium is the amount the company raised by selling its shares in the stock market at a premium to its FV.

Line 9 – Retained earnings. Every year the company earns net profit (the outcome of the P&L statement). It allocates this profit in various reserves and leaves the rest in retained earnings.

Reserves are like a pool of funds a company sets aside for a specific purpose.

Capital reserves are to fund future asset purchases, mergers, expansions etc.

General reserves are for general purposes such as additional inventory, marketing etc.

As all this money is earned and retained in the company, it increases the value of your equity share.

💡 Book value of equity share = Total value of equity ÷ Number of issued shares

Book value per share tells you how much money the company holds for every share. A strong company’s share generally trades at a price higher than its book value.

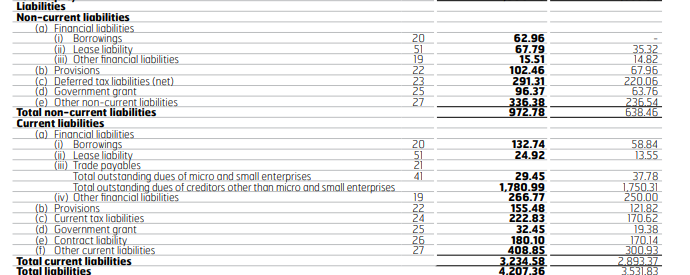

(ii) Liabilities

Liabilities are the company’s payment obligation in the next 365 days (current liabilities) and in the long term (non-current liabilities).

Financial liabilities are various types of loans that charge interest. Any principal amount of long-term loans to be repaid in the next 365 days is deducted from non-current liabilities and added to current liabilities. For instance, you took a ₹10 lakh loan for 10 years and you will be paying ₹50,000 of the principal amount in the next 12 months. Your current liabilities will appear as ₹50,000 and non-current liabilities as ₹9.5 lakhs.

This logic applies to all similar line items in current and non-current liabilities.

Provisions come from the term “provide for”. It is the amount the company sets aside for any upcoming payments, dues, or losses. It is mostly related to payments of employee benefits like bonuses and pensions.

Trade/Account Payables is the amount the company has to pay its suppliers and is associated with the daily business operations. It is a category specific to current liability.

All other line items are self-explanatory and show a company’s short and long-term obligations.

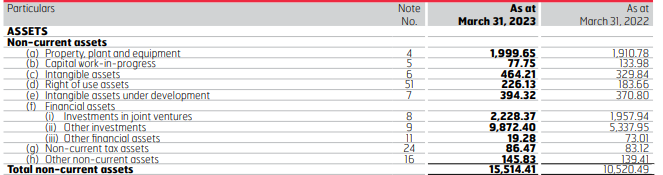

(iii) Assets

Liabilities tell you what the company has to pay. Assets tell you whether it has the liquidity to pay its liabilities.

💡 Liquidation: Liquidation is the process of converting an asset into cash.

Like liabilities, assets also have current and non-current assets. However, there is no 365-day rule in current assets. The classification is based on the liquidity of the asset.

Current assets

Current assets have specific line items like:

Cash and cash equivalents and bank balances are the most liquid assets. This line item is the outcome of the cash flow statement where we take the opening cash balance and adjust for the inflow and outflow of cash from operations, investing, and financing to determine the ending cash balance.

Trade/Accounts Receivables is the revenue the company recorded but did not receive complete payment for. These are the products sold on credit. As the company gets the payment, the Accounts Receivables amount reduces.

Inventories are the raw materials and goods stored by a company to sell in the market. Inventories can be at various stages: raw materials, work-in-progress/unfinished goods, and finished goods. Keeping the inventory requires warehousing costs and is crucial in daily operations. If an inventory gets damaged or becomes obsolete (i.e. the product lifecycle is over; for instance, medicines have passed their expiry date), the company has to write off the inventory by reporting a one-time expense.

For instance, a pharma company has an inventory worth ₹1 lakh and the medicine will expire in two days. They cannot sell this inventory anymore as it has become worthless. It will reduce the Inventory amount by ₹1 lakh from the Balance Sheet. This is called writing off the inventory. This amount of ₹1 lakh will appear as “write-off” expense in the P&L statement as the company bears the cost of obsolete inventory. Hence, companies must maintain a reasonable amount of inventory they can sell.

A company uses its current assets to pay its current liabilities. Hence, the company has to keep a fine balance between the two to ensure a smooth flow of cash in and out of the business.

Fixed assets

Any asset that is not easy to liquidate is fixed or illiquid. Some even call them “non-current assets” or “long-lived assets”.

Intangible assets are those things that you cannot touch and feel but have an economic value and help you get a royalty or premium. These include patents, intellectual property (IP), trademarks, copyrights, goodwill, etc. Many technology and pharma companies develop an intangible asset (patent). All the costs incurred to develop the product can be accumulated here as intangible assets.

In the case of Eicher Motors, it makes motorbikes and trucks. Hence, it capitalizes its product development cost in “Intangible assets under development”. This includes all the costs incurred till the bike and truck are tested and ready for mass production. When the company produces/manufactures the bike and truck, that cost is included in the P&L as the cost of goods sold.

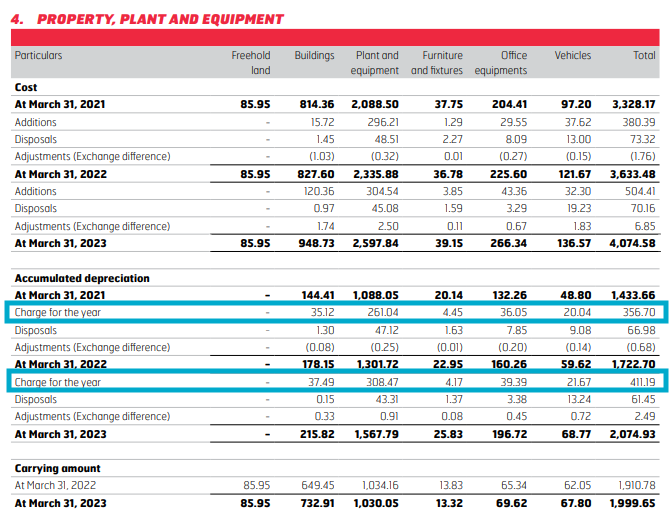

Property, plant, and equipment (PPE) purchased to perform business operations are mentioned here. But if the company purchased a building as an investment (maybe to lease it to someone else), it will be categorized under Investments. The idea is to show the assets that are in use for business operations.

Depreciation and impairment

All fixed assets have a useful life during which they contribute towards generating revenue. For instance, Eicher Motors spends its largest capital on property, plant and equipment. This is a one-time cost of thousands of crores of rupees. How can you incorporate this cost into your business? That is where depreciation comes in.

Depreciation divides the capital cost throughout the useful life of the asset. In other words, depreciation is the expected wear and tear of the fixed asset over a fixed period.

Sometimes, an asset loses its value at a faster rate because of a natural calamity or an incident. At that time, the asset is impaired (weakened or damaged). Since the asset’s value has fallen below the book value (a value that appears on the Balance Sheet), the company reduces the asset price and tags the lost value as ‘Impairment’. The company adds the Impairment amount as an expense in the P&L statement as it has to bear the cost.

For instance, Ravi spent ₹8 lakhs on a taxi that will last 10 years. He has to earn this money back from the taxi fare.

Depreciation – He will divide the ₹8 lakh cost over a 10-year period as the “depreciation cost” and recover the amount. He will deduct the depreciation amount from the asset value and add it as an expense in the P&L statement.

Impairment – One day, his taxi met with an accident and the value of the car fell to ₹1 lakh. But in the books, the depreciated value of the car is ₹5 lakhs. Ravi will incur a ₹4 lakh impairment expense from his pocket, which will reduce his profit for that year.

These long-term assets will help the company earn money to pay long-term liabilities and give returns to shareholders. Here again, the company is balancing its assets to match the liability and transfer the balance amount to owners (Retained Earnings of Shareholder Equity).

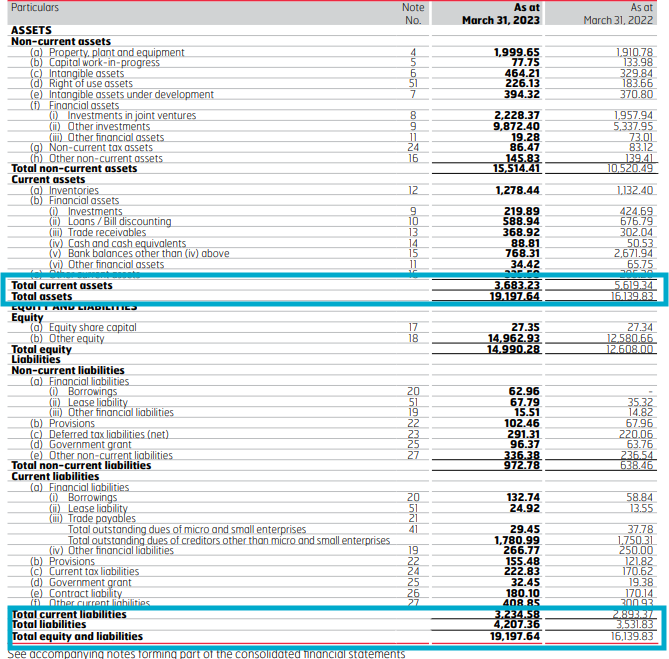

Looking at the balance sheet as a whole

Now let’s join the three parts and look at the complete Balance Sheet.

Look at the above Balance Sheet from a liquidity POV. Eicher Motors has ₹3,683.2 crores in current assets, which is enough to pay its ₹3,234.5 crores in current liabilities.

The company’s total liabilities of ₹4,207 crore are significantly lower than its Shareholder Equity of ₹14,990 crore. This shows that the company has more Owned funds than Owed funds, which means its debts are at comfortable levels.

Where all the statements intertwine

Throughout the chapter, you must have noticed some elements of P&L and cash flow statements keep popping up. It is because these daily business operations have an impact on the overall value of the company.

All three of these stories – the P&L statement, cash flow statement, and balance sheet – are intertwining at certain intervals affecting each other.

The cycle of the P&L statement: A company makes a sale, incurs operating expenses and finance costs, deducts depreciation, and adds other income from investments to arrive at the net profit. Each of the five elements of the P&L statement affects a line item in the Balance Sheet.

P&L’s Impact on the Balance Sheet

Sales for which you didn’t receive the payments change Accounts Receivable (Current Asset) and Cash Flow From Operations (CFO).

Operating expenses change Accounts Payable (Current Liabilities), Inventory (Current Asset), and CFO.

Net Profit is added to your Reserves and Surplus and changes CFO.

Balance Sheet’s Impact on the P&L

The debt (Non-current liability) a company takes or repays changes its Finance cost (interest and processing fees) and Cash Flow From Financing.

The asset (Non-current assets) a company purchases or develops is gradually expensed as depreciation (P&L).

Investments (Assets) the company makes generate returns and interest that is added as Other Income (P&L) and affect Cash Flow From Investments (CFI).

💡Tip: This whole exercise is to help you visualize how one transaction affects several line items. Try reading 5-6 Financial statements of companies in different sectors. Visualizing the transactions comes with practice.

As the company’s story unfolds, the financial statements leave the climax open to debate. Every person analyses and interprets these statements differently. If everyone could see what Warren Buffett saw in the financial statements, he wouldn’t be the billionaire investor he is today.

Now that you can read and understand a financial statement, the next step is to analyze them.

Get ready to use all that you have learned so far to analyse a company in the coming chapters.

Summary

- The balance sheet is a sheet that lists everything a business owns and owes and balances the two. Every asset is funded by a liability or business owner’s money.

- A balance sheet is used by anyone with a financial interest in the company (shareholders, creditors, suppliers, employees) to know if the company can fulfill its payment obligations and make money for shareholders.

- A balance sheet has three segments:

- Shareholder’s equity: It is the face value of the company’s equity shares and how reserves and surplus accumulated over the years enhance the book value per share. Even the owner’s fund is a liability for the company as it is obligated to give a share of its earnings to shareholders.

- Liabilities: They are loans and provisions payable in 365 days (current) and the long term (non-current liabilities).

- Assets: The current assets comprise cash, trade receivables, and inventories. If the inventory becomes obsolete or is damaged, it is written off and affects the company’s profits.

- Fixed assets include intangible assets (patent and goodwill) and tangible assets (property, plant, and equipment). The wear and tear of assets is deducted as depreciation whereas the damage to the asset is deducted as impairment and affects the company’s net profit.

- The balance sheet has to be balanced such that current assets are sufficient to meet the current liabilities. The equity and debt levels should also be balanced to ensure a smooth flow of cash in and out.